New homes won’t cure housing affordability problems

New homes won’t cure housing affordability problems – San Diego Union-Tribune - Price of New Homes significantly above the price of resales (but cheaper per square foot)

Overall Residential Real Estate Summary

Countercurrents create turbulence in the housing market, but current new construction won't help moderate housing prices, and it's not just in California. Here are the key trends in housing prices and sizes for new construction versus existing homes in California and nationally:

California:

1. Price:

- New homes in California are generally more expensive than existing homes, with a median price of $1.14 million for new construction vs. $935,000 for existing homes (22% higher).

- However, the price premium varies significantly by metro area, from 79% higher in San Jose to only 4% higher in San Francisco.

2. Size:

- New homes in California are typically larger than existing homes, with an average of 2,020 square feet for new construction vs. 1,585 square feet for existing homes (27% larger).

- The size difference also varies by metro area, from 48% larger in San Jose to 12% smaller in San Francisco.

Nationally:

1. Price:

- Nationally, new homes had a median sales price of $418,000 vs. $365,000 for existing homes (15% higher).

- However, in May 2024, new single-family homes actually sold for less than existing ones ($417,400 vs. $424,500), which is a rare occurrence historically.

2. Size:

- Nationally, new homes are typically larger, with an average of 1,990 square feet vs. 1,710 square feet for existing homes (16% larger).

- However, the size advantage of new homes has been shrinking. In 2018, new homes were nearly 500 square feet larger than existing homes, but by May 2024 this difference had reduced to just 335 square feet.

Key trends:

1. New home sizes and lot sizes are decreasing faster than those of existing homes, likely in response to affordability challenges.

2. New homes are becoming more cost-effective on a per-square-foot basis. As of May 2024, new homes sold for $3.50 less per square foot than existing homes nationally, the largest discount in at least six years.

3. The price and size premiums for new construction are generally more pronounced in California compared to national averages.

4. There's significant variation within California markets, with some areas like San Jose showing much larger price and size premiums for new construction than others.

These trends reflect builders' efforts to adapt to affordability challenges by offering smaller, relatively more affordable new homes, particularly evident in the national data. The California market, however, still shows more significant price and size premiums for new construction compared to existing homes.

New homes won’t cure housing affordability problems

This is not only a crazy California thing

“Numerology” tries to find reality within various measurements of economic and real estate trends.

Buzz: Construction is not a quick cure for homebuying affordability headaches because the bulk of the new homes being built are pricier and larger than the rest of what’s sold on the market.

Source: My trusty spreadsheet spied a Zillow study comparing existing residences sold in May with newly constructed ones in 46 big US metropolitan areas – including six in California.

Fuzzy math: Developers argue they need to build bigger homes to make the expensive land they buy, plus other construction costs, pencil out financially.

Topline

Yes, it’s only one month of sales, however, think about California through the median results for the six cities studied.

Buyers paid $1.14 million for new homes vs. $935,000 for existing ones. So what’s being built is 22% pricier.

Now some of that premium price can be tied to mortgage rate discounts offered by builders that allow house hunters to pay up for new homes.

But the bulk of those higher prices are because builders typically sold a 2,020-square-foot house vs. 1,585 for existing ones. So the new stuff is 27% larger.

Please note that this is not only a crazy California thing.

Nationally, new homes had a $418,000 median sales price vs. $365,000 existing – that’s 15% higher.

Amd US homebuyers typically got 1,990 square feet new vs. 1,710 for existing homes – 16% larger.

Details

Ponder the new vs. “used” patterns within California, ranked by the price premium builders got …

San Jose: $2.87 million median for new construction vs. $1.6 million for existing homes – 79% higher (the fourth-biggest gap of the 46 metros). That bought 2,360 square feet new vs. 1,600 existing – or 48% larger (No. 4).

Sacramento: $745,920 median new vs. $575,000 existing – 30% higher (No. 24) for 2,340 square feet new vs. 1,670 existing – 40% larger (No. 8).

San Diego: $1.14 million median new vs. $900,000 existing – 27% higher (No. 25) for 2,060 square feet new vs. 1,480 existing – 39% larger (No. 10).

Los Angeles-Orange County: $1.15 million median new vs. $970,000 existing – 19% higher (No. 27) for 1,970 square feet new vs. 1,520 existing – 30% larger (No. 16).

Inland Empire: $610,805 median new vs. $562,500 existing – 9% higher (No. 32) for 1,980 square feet new vs. 1,720 existing – 15% larger (No. 30).

San Francisco: $1.27 million median new vs. $1.23 million existing – 4% higher (No. 38) for 1,380 square feet new vs. 1,570 existing – 12% smaller (No. 46).

Bottom line

This is not just a greedy builder problem.

In large part, these pricing gaps are the result of a host of policy and marketplace challenges that make it far easier to produce high-end housing.

Fancy and expensive new communities are simpler to sell politically in the local regulatory process.

And that premium housing can be sold to wealthier clientele. Those sales usually produce fatter profit margins.

Catering to the upper crust can be a smoother sell to the investors and bankers who put their dollars behind construction plans. And so far in recent years, there are enough folks with deep pockets willing to gobble up the more expensive new offerings.

Peek at the 10 US metros in Zillow’s study with the smallest new-to-existing price gaps. These markets essentially had little difference in price or size of these two homebuying options.

Yet in the 10 with the largest gaps, new homes were typically 40% larger compared with new homes – and 80% pricier. (FYI: Those 10 markets, a surprising group: Columbus, St. Louis, Kansas City, Philadelphia, Detroit, Milwaukee, Cleveland – and San Jose, New York, and Miami.)

Look, there are no simple solutions to fix homebuying’s dramatic “unaffordability” problem. And relying on the easy answer – build what’s convenient – won’t work.

Yes, any new supply of housing at no matter the price point does ease inventory imbalances.

But it’s a darn slow process for noteworthy affordability improvements to trickle down from housing’s high end to help the most-stressed house hunters merely seeking a modest place of their own.

Jonathan Lansner is business columnist for the Southern California News Group. He can be reached at jlansner@scng.com

Originally Published:

As new construction homes adapt to affordability challenges, they offer a renewed value proposition.

- New homes sold for $3.50 less per foot than existing homes in May, the largest discount in at least six years.

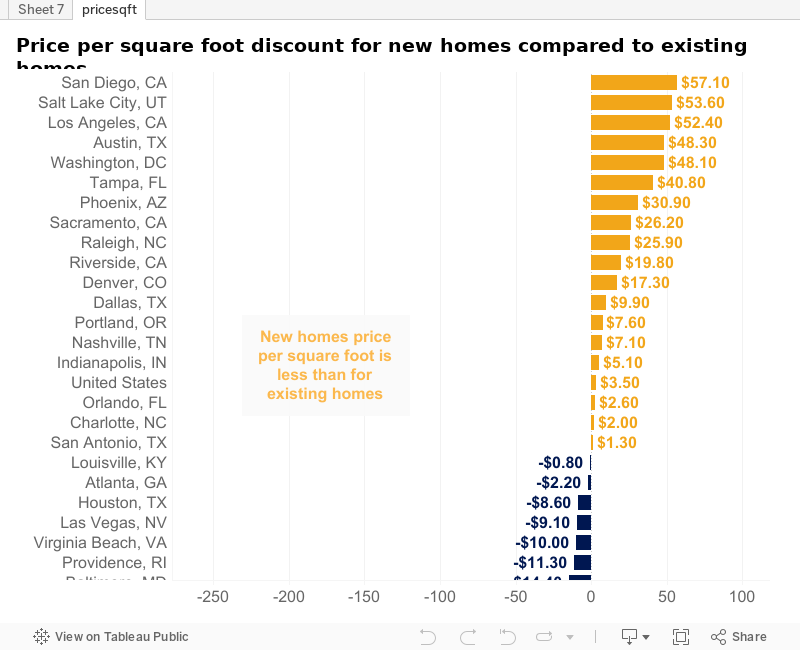

- San Diego, Salt Lake City, and Los Angeles offer the biggest discount for new builds.

- Not needing updates or repairs was the top reason for choosing a new home, buyers say.

- Lot sizes and square footage for new homes have fallen significantly over the past six years.

New construction homes commanded a serious premium before the pandemic – from $15 to $22 more per foot than existing homes – but they now represent a relative value. Buyers of new homes got a $3.50 discount per square foot in May compared to those purchasing existing homes. That’s the biggest discount in Zillow median sale price data that stretches back to 2018.

While new-build properties are still selling for about $54,000 more than existing homes, buyers are now seeing savings by the foot nationwide and in 21 major metros – beyond incentives commonly offered by builders. New construction homes in May sold for $209.70 per square foot nationally, just under the $213.20 rate for existing homes.

New builds have only been less expensive per square foot than existing homes in five other months since the start of 2018, and this is the biggest savings seen yet. Builders are offering more price cuts than homeowners selling their own properties. About 29% of new homes received a price cut in June. Meanwhile, more than half of all builders (61%) offer sales incentives other than price cuts, such as mortgage rate buydowns and covering closing costs, which can save buyers thousands of dollars over the first few years of ownership.

Composition considerations

The new construction homes of today, their lot sizes, and the share that are detached vs. condos have evolved over recent years, all contributing to changing the math when comparing prices against existing homes. Today’s new construction buyers are getting significantly smaller lots than those in prior years, and the lot-size advantage of buying existing homes is growing.

Existing home sale prices are up 52% since before the pandemic, while the sale price of new builds has risen by just 26% over the same period.

Zillow listings data shows new construction lots are shrinking far faster than existing ones. The average lot size for new builds is now 460 feet smaller than in 2018 (about the size of a one-car garage), while lots of existing homes shrank by just 94 square feet.

That’s widened the gap in lot sizes between new homes and existing homes. Buyers of existing homes enjoy lot sizes 1,900 square feet larger, on average, than those purchasing new builds – up from a difference of 1,535 feet in 2018.

Land costs continually rise as buildable land becomes more scarce – making more efficient use of the space is one way for builders to make sure housing is still within reach as costs rise.

In May of 2018, new homes that sold were nearly 500 square feet larger than existing homes that sold. But that size advantage shrank in May of 2024 to just 335 square feet.

Home sizes are falling faster for new builds – those sold in May are 185 square feet smaller than in 2018 – the size of a decent bedroom – compared to just a 24-foot drop over the same period for existing homes that sold.

Context is important here. When mortgage rates doubled in 2022, costs skyrocketed for both builders and their buyers, pushing developers to pivot toward smaller units. This is in response to the massive housing shortage and affordability crisis that has pushed homeownership out of reach for many households.

Another explanation for why the gap in price per square foot shrank and – for now – reversed, is that condos and townhomes represent a far smaller portion of new construction sales than they did in 2018. Condos represent just 3% of all the new construction units sold in May 2024, versus 10% in 2018. Condos are significantly more expensive per square foot of living area than single-family units are, so by making up a smaller portion of the mix, price per square foot should ease accordingly.

The more cyclical nature of the existing-home sales season is another factor affecting prices, and price per square foot by extension. Home price growth of existing homes typically peaks in the spring – growth is already cooling down in June from a May peak. Price growth for new-build homes typically has less seasonal variation.

New construction has taken on added importance by providing much-needed inventory while homeowners are still, in large part, locked in to their existing low-rate mortgages. Home construction took off during the pandemic but so far hasn’t made up for years of underbuilding.

The nationwide housing shortage grew to 4.5 million homes in 2022, according to new research from Zillow. Zillow’s latest market report shows the number of existing homes for sale on the market is still 33% below pre-pandemic levels nationally, and the deficit is far greater in many markets.

New build buyers want less hassle, within the budget

About two in five new construction buyers (43%) said the top reason for choosing a new build was that the home was move-in ready, without any need for repairs or updates, according to Zillow’s New Construction Consumer Housing Trends Report.

Affordability and relief from the heat – two top topics of the times – weigh heavily on the minds of buyers when considering their next home’s most important features. A home within their budget was very or extremely important to 89% of new-build buyers – the same share that said the same thing about air conditioning. That a home is energy efficient was the third most important factor.

Updated June 27, 2024

11:01 AM EDT

ynesher / Getty Images

- New single-family homes were cheaper than existing ones in May, a historically rare occurrence.

- Existing home prices are hitting record highs amid elevated mortgage rates as the "lock-in effect" restricts supply.

- Lower median new home prices may reflect builders selling smaller, cheaper homes that buyers can actually afford.

If you’re in the market for a single-family house and want to save a few bucks, you might want to try building a new one from scratch instead of buying an existing one.

The median price for a newly built single-family house sold in May was $417,400 according to the Census Bureau, while the median single-family existing homes sold for $424,500, data from the National Association of Realtors showed. Existing homes costing more than new builds is a rare occurrence—it’s only happened in 14 months since 1968, most recently in 2021, and only twice since 1982.12

To be sure, the numbers aren’t 100% comparable—they’re gathered using different methodologies—but they do illustrate a trend. New home prices have fallen since peaking at a median $460,000 in October 2022, possibly because builders have tried to build smaller, cheaper houses that buyers can afford amid mortgage rates close to their highest in decades.

Meanwhile, existing home prices have been pushed to record highs as high mortgage rates have discouraged sellers from putting their houses on the market, restricting for-sale listings and keeping competition fierce.

The fact that new homes are cheaper than used ones serves as “a sign of how contorted the housing market is,” Robert Frick, corporate economist with Navy Federal Credit Union, wrote in a commentary.

Update, June 27, 2024— This story has been updated to further clarify that the prices given for existing and newly-built homes are for single-family units.

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

Hidden Price of New Construction

Mello-Roos Tax Districts: Pros & Cons for California Home Buyers

In This Article

In this guide: An explanation of the “Mello-Roos” taxes in California affect on home buyers, including the pros and cons of buying in such a district.

You’re in the market to buy a home in California. You find a home in a nice neighborhood that meets your needs and falls within budget, so you’re eager to make an offer.

But your real estate agent tells you that this home is located in a Mello-Roos district and therefore has high property taxes.

Wait … what? What is a Mello-Roos tax in California? Why do some neighborhoods have these additional taxes while others don’t? And how might it affect your property tax bill if you decide to buy a home in such a neighborhood? Ultimately, how do Mello-Roos taxes in California affect home buyers?

Those are just some common questions home buyers ask about Mello-Roos taxes. And we will tackle all of them (and more) throughout this home buyer’s guide.

Mello-Roos: A Property Tax ‘Add-On’ in California

When buying a home in California, you might encounter what’s known as a “Mello-Roos districts.” Also known as a Community Facilities District (CFD), they’re a common sight within the California real estate market, especially in the newer communities. [and most new construction]

A Mello-Roos tax is a special assessment added to your property tax bill. It’s used to fund new infrastructure and amenities within a specific development, neighborhood, or community. This particular tax is unique to California, but other states have their own versions.

“Mello-Roos” comes from the two California politicians who sponsored the Community Facilities Act of 1982: Senator Henry Mello and Assemblyman Mike Roos. This act gave local governments and developers in California a new way to raise funds for infrastructure and amenities in specific communities.

It also allowed them to circumvent property tax limitations put in place by previous legislation. How? Because a Mello-Roos is technically a “parcel tax.”

Unlike a traditional property tax, which is based on the assessed value of your home, a parcel tax like Mello-Roos is based on characteristics of the property itself. It might be based on things like square footage, lot size, property type, etc. It might also be a flat rate applied to all parcels within the district.

What California Home Buyers Need to Know

In California, Mello-Roos districts often entice home buyers with promises of top-notch schools, beautiful parks, and well-maintained roads. And that might be true, for the most part.

But a savvy home buyer will want to know if the benefits of Mello-Roos are worth the long-term financial commitment. In short, you must figure out what you get for your money.

To determine this, you’ll need to understand the pros and cons of Mello-Roos districts in California from a homeowner’s perspective. So, let’s explore some of those pros and cons.

Pros of Mello-Roos Districts

- New and Improved Infrastructure: Mello-Roos taxes directly fund projects like modern schools, expansive parks, updated roads, libraries, fire stations, and more. These amenities can improve the quality of life for residents while boosting property values at the same time.

- Faster Housing Development: When local governments lack immediate funding for infrastructure, Mello-Roos allows developers to get projects off the ground.

- A Sense of Community: Residents of Mello-Roos districts often enjoy well-manicured neighborhoods and attractive common areas. This can foster a greater sense of community and pride.

Cons of Mello-Roos Districts

- The True Cost: In California, Mello-Roos taxes can be substantial. Home buyers in these districts can have hundreds or thousands of dollars more added to their annual property tax bills. And unlike standard property taxes, Mello-Roos is not tax-deductible. This creates an additional financial obligation as long as you live in the neighborhood.

- Resale Challenges: When it’s your turn to sell, be aware that added costs can shrink the pool of potential buyers. Some buyers will balk at Mello-Roos, which might lengthen your time on the market or influence your ultimate sale price.

- Lack of Direct Control: While paying for new facilities, there is often limited direct voter oversight on how Mello-Roos funds are managed. In some communities that have these taxes, concerns have been raised about transparency and possible mismanagement.

How Much Are Mello-Roos?

Unfortunately, there is no standard tax rate for Mello-Roos districts in California. So you’ll have to look it up for each community where you’re considering buying a home. The tax rate can vary significantly from one district to another.

More than any other factor, the cost of the infrastructure or services being funded by the Mello-Roos district will determine the tax rate. A larger, more ambitious project (like multiple schools and parks) will bring a higher rate than a district focused on simpler necessities.

The tax burden spread out could be based on how big your house or lot is, the type of property, or even a simple flat rate for everyone.

According to the California Title Company:

“In general, the special taxes and assessments do not exceed 1% to 1.5% of the market value of new homes. Moreover, all annual taxes (including property tax) usually do not exceed 2% to 2.5% of the home’s market value.”

But there’s plenty of transparency here. Potential home buyers within a California Mello-Roos district must be given detailed information about the tax rate, projected increases, and future obligations. Full disclosure is required by law.

Tips for Making an Informed Decision

So, is it worthwhile to buy a home in California in a Mello-Roos district?

There isn’t a clear yes-or-no answer to this question. Every home-buying scenario is different because there are many variables involved. As a buyer, you must weigh the specific benefits against the additional costs.

Here are some questions to answer before buying a home in a Mello-Roos district:

- What exactly does my Mello-Roos tax pay for? (Get a thorough list of funded projects, such as schools, parks, infrastructure, etc.)

- How much is the current tax, and what is the maximum future amount allowed?

- How long will the Mello-Roos payments last? Is there a set end date or expiration?

- How is the tax calculated? (Is it based on my house/lot size, a flat rate, etc.?)

- How does this Mello-Roos tax impact my overall affordability? (Factor it in as if it were an additional part of your mortgage payment [but it will never be paid off, unlike your mortgage].)

- Is there a record of responsible financial management within the district?

- Will I have direct oversight or a say in how the Mello-Roos funds are used?

As with other real estate-related decisions, a little research goes a long way!

How HOA Fees Work in New-Construction Communities: What To Expect

When purchasing a new-construction home, most buyers prepare for the down payment, closing costs, and subsequent monthly mortgage payments. But one additional expense that sometimes gets forgotten in initial calculations is homeowners association (HOA) fees.

These “neighborhood dues” are generally paid monthly, quarterly, or annually and go toward the upkeep and preservation of the community where a home is built.

The money might go toward ongoing expenses like landscaping and pool cleaning, but it could also be used for bigger ticket items like the maintenance and staffing of a community pickleball court. Basically, it’s everyone chipping in to make sure any common-area expenses are covered.

Here’s more of what homebuyers, homeowners, and home sellers need to know about HOAs in a new-construction community.

The benefits of an HOA

The overwhelming majority of people who live in a community with an HOA (89%) rate their overall experience as positive, according to the 2022 Homeowner Satisfaction Survey conducted by the Foundation for Community Association Research.

Beyond extra amenities, it’s important to remember that HOAs also ensure the aesthetics and safety of the community.

“Homes [in HOA neighborhoods] are going to be uniform, landscaping will be kept up, there are security gates or fencing, and you’re not going to have a neighbor who paints their home a bright neon orange with dead plants and grass and hundreds of lawn sculptures,” says Doug Jacobs, builder partner manager at Opendoor.

“An HOA enables you to maintain the value and continuity of the neighborhood while also protecting your investment in your home,” adds Jacobs.

HOAs also alleviate for homeowners the hard work of keeping their community looking and functioning at its best. Not only is that great for the time you’re living there, but it also helps protect the resale value should you decide to move.

How are HOAs in new-construction communities created?

New-construction HOAs are usually determined by the builder and an HOA management company during the development phase of the community, prior to selling lots.

“The management company will work with an attorney on drafting the bylaws (how the board of directors will govern) as well as the covenants, conditions, and restrictions (CC&Rs), which are essentially the rules and regulations for the homeowners,” says Tiffany Sears, a broker and agent of The Sears Group in Charlotte, NC.

At

this developmental point in the new-construction process, any HOA fees

for homebuyers are calculated based on operating costs and expenses for

the community, taking into consideration planned amenities (like

swimming pools and gyms) and expected maintenance of the common

community areas (such as parking lots and security gates). [Many times the builder will try to set the HOA fees below what long term maintenance will require in order to enhance saleability, and fees will have to be raised after the development sells out and the builder has left the picture. This may also lead to substantial assessments for defered big ticket maintenance items. Make sure quoted fees are reasonable.]

Since HOA dues will add to overall monthly expenses, buyers will need to know what those fees are at the time of signing the contract on a new-construction home.

“Most builders will provide the bylaws and CC&Rs so the buyer can review the rules and regulations to make sure they aren’t buying something that has conditions that they can’t or don’t want to adhere to,” says Sears.

How much are HOA fees?

Fees vary widely depending on where the community is and the scope of the amenities offered.

“Nationwide, the average monthly HOA fee is between $200 and $400, but they can also run into the thousands of dollars if you’re in a luxury gated community that’s in a sought-after location,” says Jacobs. “The more ‘amenitized’ the community is, the higher the HOA fees are going to be.”

The HOA management company is also paid for by the HOA fees, and most communities also charge a “capital contribution.” This fee is assessed at closing and is a part of the closing costs the buyer pays.

“I like to call it a ‘welcome to the neighborhood gift,’ essentially building the HOA’s savings account,” says Sears. “It is designed to be a fee to help build the operating fund for the HOA for any large projects that might need to be covered over the years.”

Are HOA fees ever negotiable?

Since HOA dues are calculated and paid differently (with billing usually coming directly from the HOA management company), this fee is typically not up for haggling.

“The real estate industry likes to say that everything is negotiable, but when it comes to HOA fees, it’s very unlikely that they can be negotiated down,” says Jacobs.

However, there is a possibility that HOA fees can be negotiated with a new-construction builder to have them be offset as an incentive.

“I have seen builders include the first year of dues as an incentive to purchase,” says Sears. It never hurts to ask.

Can I opt out of an HOA?

HOA and their fees are not “participation optional.” If you buy into a neighborhood that has one, you are required to pay your part.

“You typically cannot choose to pay for only some of the amenities, as your portion of the budget for HOA fees covers all of the amenities,” says Jacobs.

The one caveat here is that sometimes, there will be “levels” of participation.

“Many new-construction communities offer a variety of amenities, but not all of them may be included within the HOA fees. There may be some amenities that can be chosen for an added cost beyond the base HOA fee,” says Chris LaMont, an American Standard Homeowning 01 featured instructor and star of the HGTV show “Buy It or Build It.”

For example, with communities that have amenities like boat dock access, a country club, or a golf course, the HOA might be for only the public areas and buyers would have to elect to join those additional amenities.

“I have seen communities that have two different HOA dues where one is for the upkeep of the community and the second one is for access to the pool, playground, or clubhouse amenities,” says Sears.

How do HOA fees factor into financing a mortgage for a new-construction home?

Mortgage lending guidelines evaluate HOA fees when determining how much to lend to a borrower.

“HOA dues are considered a recurring debt and are calculated as a part of your debt-to-income ratio by mortgage lenders, and this may affect a prospective buyer’s loan approval amount,” says Sears.

If a potential homebuyer is at the top of their DTI ratio, high HOA fees could actually make a property financially unavailable.

During the loan approval process, a buyer should ask the lender if there are any concerns related to an HOA amount to be aware of.

“As a real estate agent, this is one question I always ask because we want to avoid any issues where a buyer falls in love with a home, but the HOA makes it out of reach for them,” says Sears.

Do HOA amounts ever go up?

HOA fees can change on an annual basis. For example, maintenance contracts for the common areas and insurance costs to protect the property are often renegotiated yearly. Also, there might be a shortfall in funds for a higher-than-expected maintenance item that could require an increase, such as stormwater pond maintenance or tree removals.

All HOA rules and guidelines are in the CC&Rs (financial and otherwise), and people looking to buy in should review them fully.

“CC&Rs are publicly recorded and are not separable from the deed, so they’re publicly available at every local government municipality,” says Jacobs.

What happens if I can’t pay my HOA dues?

Unpaid mandatory HOA dues can lead to a lien being placed on the home and eventual foreclosure, so you must make sure you are able to pay your dues before putting down a deposit in a new-construction community.

“Make sure you set an annual budget outside of your mortgage payments to cover HOA fees and know that these costs are subject to change year over year,” says LaMont. “These fees shouldn’t be taken lightly, as there can be harsh repercussions for unpaid dues, fines, and any accumulated interest.”

Comments

Post a Comment