California Property fire insurance in transition as Rates Increase and Policy Availability Declines - Does Prop 103 need rewrite?

|

Map of Insurer-Initiated Nonrenewal Rate in California in 2019 by ZIP Code |

California fire insurance: FAIR Plan going through growing pains - CalMatters

|

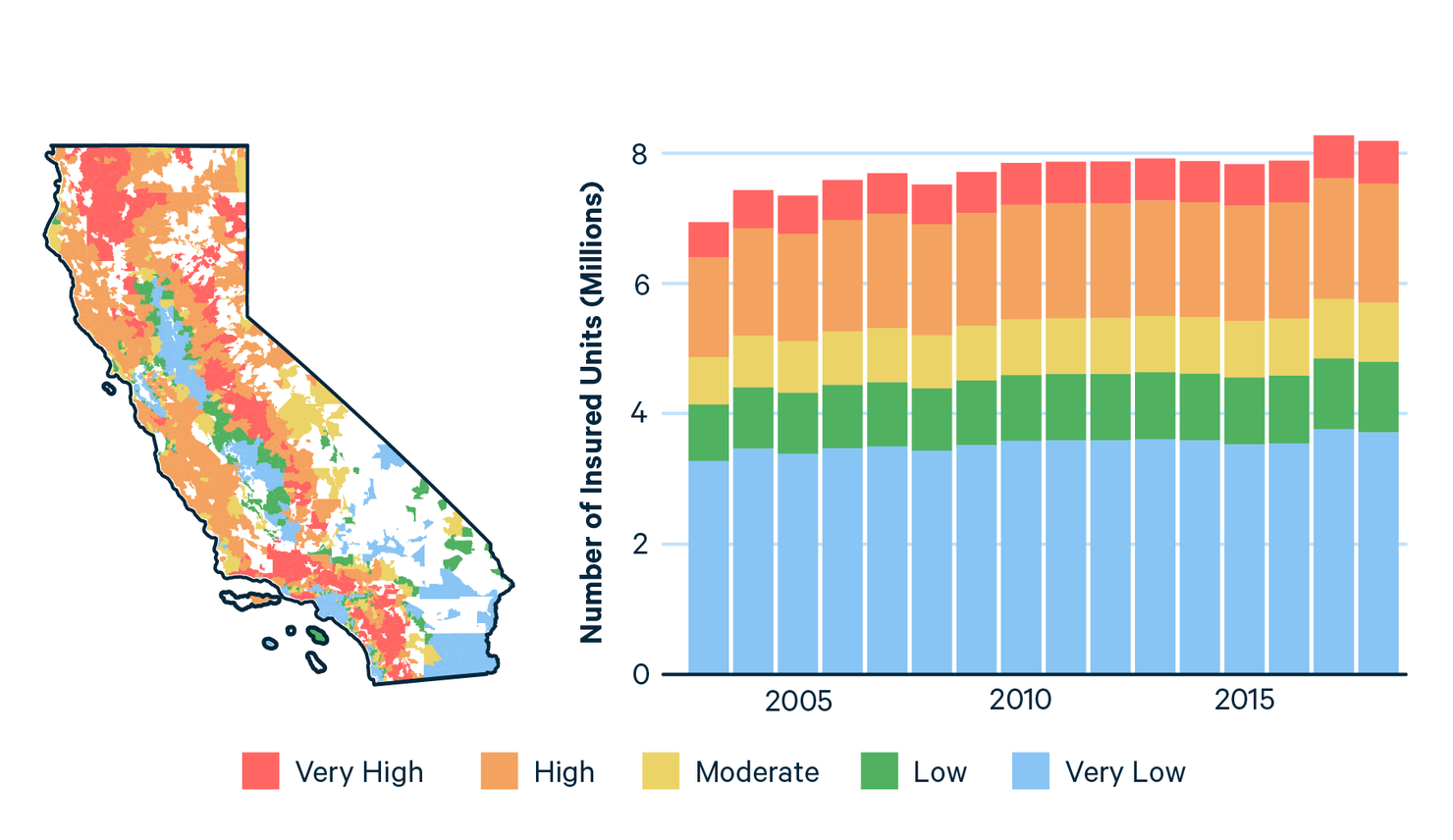

Market Share of FAIR Plan Policies in California by Fire Risk Category, 2003–2018 |

|

Premium Increase Percentage, 2003–2018, in California |

Insurance Availability and Affordability under Increasing Wildfire Risk in California

In summary

As the FAIR Plan writes more fire-insurance policies, homeowners complain about poor service, rising costs and threats of getting kicked off.

The fire-insurance premium for Bill King’s home has risen 145% since 2017 — from $399 to $979 — under the California FAIR Plan, the state’s last option for homeowners seeking fire insurance.

Add that to the increase in his auto-insurance premium, and King, who lives in Running Springs in the San Bernardino Mountains, is worried.

“What do I do?” asked King, a retiree who will turn 70 years old this summer. “Do I move out of California? At some point I’m going to have to look at things… Will I be able to face future increases depending on how long I’ll live?”

A former Orange County employee, he said he’s having a tough time wrapping his head around the situation: “It’s hard when you’ve planned your retirement and your insurance company comes along and threatens your economic well-being.”

King’s story is similar to that of other property owners who have turned to the FAIR Plan as many insurers have stopped issuing fire insurance in the state, citing climate risks and inflation. As the FAIR Plan has exploded in size — from 126,709 policies in 2018 to more than 350,000 today — homeowners and insurance brokers say they are now facing problems such as delays in mortgage closings, or homeowners losing their coverage.

Recently, King found he was unable to pay for his policy renewal online, as he usually does. He couldn’t email the FAIR Plan because the plan’s website does not provide an email address. Instead, the website tells homeowners to contact their insurance brokers. King’s broker found out that he had been assigned a new policy number without his knowledge. He barely had time to send a payment via his broker, putting him dangerously close to cancellation. Based on his individual experience, King has concluded that the FAIR Plan “is doing everything it can to help policies lapse.”

The FAIR Plan Association, a pool of insurers required by state statute to provide fire-insurance policies when property owners can’t find them elsewhere, is experiencing major growing pains.

The California Insurance Department, which under state law has oversight over the FAIR Plan — including approving its requested rate changes — in 2020 investigated consumer complaints about non-renewals and cancellations. But even after an agreement late last year that included the FAIR Plan vowing to change some of its practices, there continue to be fresh signs of turmoil.

The plan is supposed to be a temporary solution as well as a last resort for property owners, but many people, like King, have been buying insurance through the association for years.

Hilary McLean, a FAIR Plan spokesperson, said the number of policy-holders who stay on the plan has increased over the years; 90% of current FAIR Plan customers are renewing their policies for another year.

The Insurance Department has proposed new regulations, expected to be finalized at the end of the year, to try to get insurers to resume writing fire policies in the state again. But it could be a couple of years until that happens, so the FAIR Plan is likely to continue growing, which could threaten its solvency because it is taking on additional high-risk policies.

“It’s clear that a growing FAIR Plan is a problem for all Californians because of the solvency risks from a major wildfire,” said Michael Soller, spokesperson for the Insurance Department, in an email. “The commissioner’s strategy is focused on returning people to the normal market from the FAIR Plan.”

Last year, lawmakers concerned about the solvency of the FAIR Plan tried to find a legislative solution to address it and other concerns about the state’s insurance market, but no lawmaker sponsored a bill to do so.

A copy of the proposed bill language, seen by CalMatters last week, shows it would have allowed the FAIR Plan to pay for claims by issuing bonds through the California Infrastructure and Economic Development Bank, which provides low-cost financing to state and local government entities. Although the FAIR Plan is not a state entity, the bill would have deemed it “in the public interest” for the FAIR Plan to qualify for financing through the bank.

FAIR Plan President Victoria Roach refused to speak on the record for this story. Spokesperson McLean said the association is dealing with an onslaught of new applications — about 900 a day, down from 1,000 a day last November but up from 350 a day in December 2022. Incoming phone calls nearly doubled over the last half of 2023, to more than 50,000 phone calls a month. The association has hired more people, bringing the number of staff to more than 200 employees plus 80 temporary workers, to help handle the additional workload.

Making matters worse, at the end of last year the FAIR Plan went ahead with long-planned changes to its software system, leading to confusion. McLean acknowledged that led to some homeowners getting kicked off the plan — or as King describes his case, almost getting kicked off — for payment issues.

Georgia, a Placer County homeowner who requested that her last name not be used for privacy reasons, said that in mid-December, her insurance broker informed her the day her premium was due that her payment had not been received, even though the money was in escrow and she later found out that her mortgage company had already paid it. The result: She, her husband and their three kids had to part with $2,380 right before Christmas to pay their premium because they didn’t want to risk losing fire insurance.

“That was my car payment, Christmas, everything we had,” she said. Her broker, mortgage company and the FAIR Plan told her she would get her money back on Jan. 5, she said, but added that she has yet to receive it.

Meanwhile, insurance broker Tyler Nelson said the new system caused delays that led to his clients losing out on loans for homes in escrow. Nelson said he would call the FAIR Plan, wait on hold for three hours and get no help. The new system, called Duck Creek, is “the most awful thing I’ve literally ever dealt with,” he said in an email.

The FAIR Plan would not discuss individual cases and complaints. McLean said the association notified brokers that they were adopting a new system, and offered them training and help. She also said the plan has made changes that “have greatly reduced delays and otherwise improved service levels.”

“In the very rare instance of a policy being canceled in error, the FAIR Plan works diligently to resolve the issue and restore coverage per the customer’s original policy agreement,” she added.

Soller, the spokesman for the Insurance Department, said consumers should contact the department if they have trouble getting coverage from the FAIR Plan.

Even before the FAIR Plan’s software transition, Ann Avalos lost her Auburn home’s fire-insurance policy in 2021 because of a payment issue after her mortgage was sold to another company.

The FAIR Plan “didn’t contact anyone until days before they dropped me,” she said, and refused to give her a grace period or reinstate her. “No communication, customer service, compassion,” she added. Her only recourse was to reapply for another policy, and she said her $2,257 annual premium increased to $3,481. Last year, she said it rose again, to $3,686. And because she can’t get fire insurance anywhere else, she has no choice but to accept the price increases.

Asked to respond, McLean said: “FAIR Plan policy agreements detail customer responsibilities… these responsibilities are consistent with industry standards, such as on-time payments and maintaining the structural integrity of the dwelling.”

“Why wouldn’t they drop you?” Avalos asked, noting that the association’s members are the insurers themselves. “Now they have the opportunity to double what they charge you.”

“We disagree with this characterization,” McLean said. “FAIR Plan rates are approved by the California Department of Insurance and rates are the same for new policyholders and renewing customers.”

The agreement reached by the Insurance Department and the FAIR Plan in November over complaints of non-renewals and cancellations between 2016 and 2019 has led the plan to make changes. One of them is to allow policy-holders to pay a surcharge if there’s a fixable issue on their property, instead of citing it as a reason to cancel their plan. Once the issue is taken care of, the surcharge is canceled. Soller, speaking for the state Insurance Department, said that because of the agreement, the FAIR Plan “should be making it easier, not harder,” for homeowners to renew their plans.

As King thinks about his own insurance worries and his future in California, he has also had to contend with FAIR Plan premium increases for his local church, where he is an associate pastor. A couple of years ago, he said, the fire-insurance premium for the church’s main building doubled from $4,000 to $8,000.

“That’s a lot of money for our little church,” he said, noting that the church’s annual budget was less than $70,000. So instead he shopped around and found a business policy that included fire insurance, which is costing the church about $6,000. “Insurance at times seems like a great evil perpetrated upon us,” he said.

|

The Number of Housing Units Insured in California by Fire Risk Category, 2003–2018 |

|

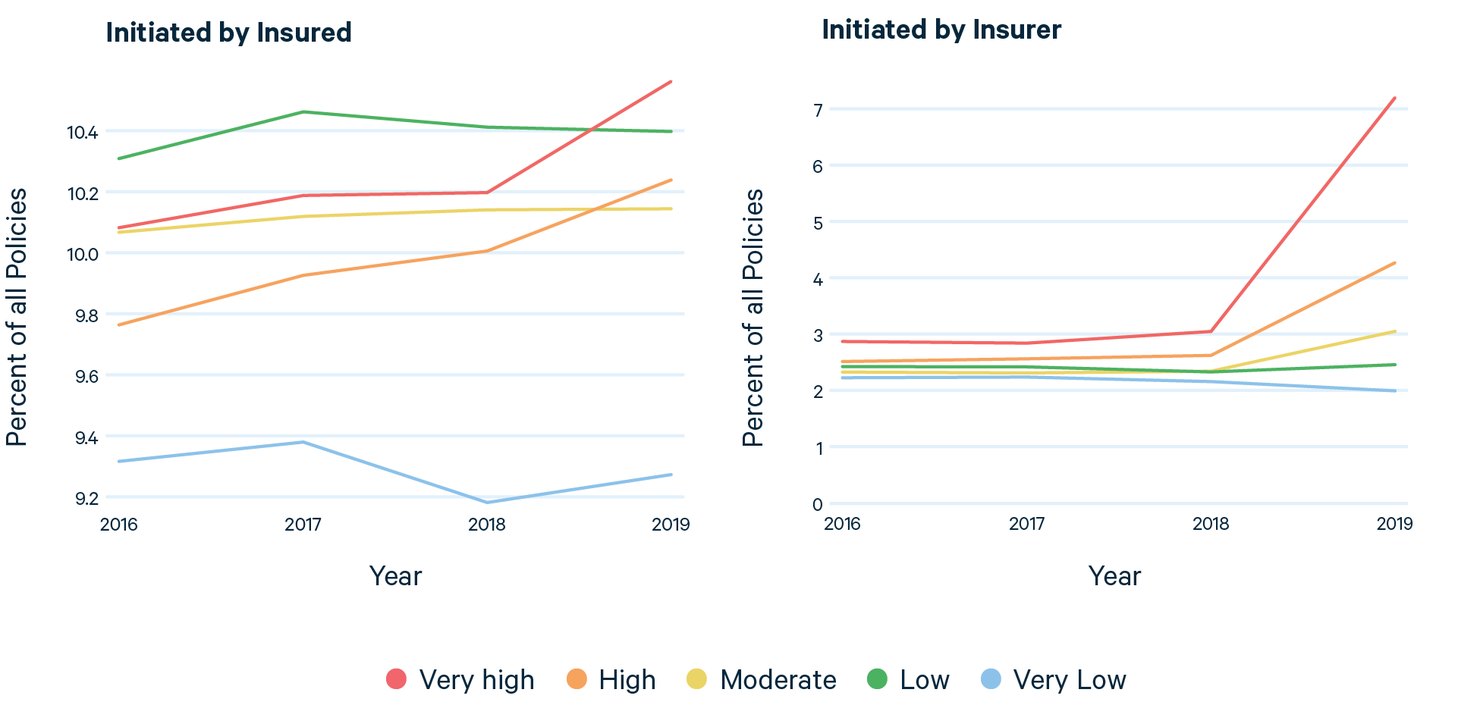

Insurance Nonrenewals Initiated by Insurers in California by Fire Risk Category, 2016–2019 |

Things to know about California's new proposed rules for insurance companies | AP News

ADAM BEAMSACRAMENTO, Calif. (AP) — Months after California’s home insurance market was rattled by major companies pausing or restricting their coverage, the state’s top regulator said Thursday that he would write new rules aimed at persuading insurers to continue doing business in the nation’s most populous state.

Seven of the 12 largest insurance companies by market share in California have either paused or restricted new policies in the state since last year.

Some state lawmakers tried to come up with a bill that would address the issue. But they failed to reach an agreement before the Legislature adjourned for the year last week.

Here’s a look at what California Insurance Commissioner Ricardo Lara proposed and how it would affect the state’s insurance market:

WHAT ARE THE RULES FOR INSURANCE COMPANIES?

Unlike most states, California heavily regulates its property insurance market.

In 1988, California voters approved Proposition 103. It said insurance companies had to get permission from the state Department of Insurance before they could raise their rates.

When setting their rates, insurance companies cannot consider current or future risks to a property. They can only use historical data.

Insurance companies also buy insurance themselves, a process known as reinsurance. Companies are not allowed to consider their reinsurance costs when setting rates for California homeowners.

WHAT IS THE PROBLEM?

Climate change has intensified wildfires in California. Of the 20 most destructive fires in state history, 14 have occurred since 2015, according to the California Department of Forestry and Fire Protection.

Insurance companies say that because they can’t consider climate change in their rates, it makes it difficult to truly price the risk for properties. They also complain that they are having to pay more for reinsurance, which they cannot recoup from ratepayers.

Many insurers have responded by pausing or restricting new business in the state. They’ve also opted to not renew insurance coverage for some homeowners.

When homeowners who need insurance can’t get it from private insurance companies, they must purchase policies from the California Fair Access to Insurance Requirements (FAIR) Plan. The plan is primarily funded by policies sold to customers. Insurers only pay into the fund if it is insolvent or to keep it from going insolvent.

The number of people on the FAIR Plan has nearly doubled in recent years. Insurance companies are worried about this trend. If the fund were to go insolvent, insurance companies would have to cover the cost.

WHAT IS THE STATE’S PLAN?

California Insurance Commissioner Ricardo Lara said he will write new rules that would let insurers consider climate change when setting their rates. He has also pledged to consider rules that would let them consider some of their reinsurance costs.

The rules requiring insurance companies to get permission from the state to raise their rates would not change.

Lara said the state will only let companies use these new rules if they write more policies for people who live in areas threatened by wildfires. He said this means companies must write policies in these areas of no less than 85% of their statewide market share. That means if a company insures 20 out of 100 homes, the company would have to also write 17 policies for homeowners in an area threatened by wildfires.

HOW WILL THIS AFFECT RATES?

Some consumer groups, including the California-based Consumer Watchdog, fear that allowing insurance companies to consider climate change in their rates will lead to dramatically higher prices for homeowners.

But Lara said the new rules could also benefit homeowners. He said insurance companies could also consider improvements that owners have made to make their homes more resistant to wildfires. Companies could also consider the billions of dollars in public money that the government has spent to better manage forests and reduce wildfire risks.

If the rules work and more companies stay in California’s insurance market, it could increase competition for customers — potentially holding rate increases in check.

WHEN WOULD THE RULES TAKE EFFECT?

It would take a while for state regulators to write the rules. The process includes lots of time for insurance companies and consumer groups to give their input. Lara said he has given the department a deadline of December 2024 to have the new rules completed.

Rethinking Prop 103’s Approach to Insurance Regulation - International Center for Law & Economics

ICLE White Paper

Executive Summary

California voters passed Proposition 103 in 1988. Since that time, California’s insurance market has struggled to keep pace with national trends and product innovations. The problems with the regulatory regime Prop 103 created most recently came to a head with the Sept. 21 announcement by Gov. Gavin Newsom that he had issued an emergency executive order to stabilize the state’s rapidly deteriorating market for property insurance.

As other states consider the adoption of reforms inspired by Prop 103, it is necessary to revisit the law’s genesis and recent history, as well as to examine the problems that it has fostered.

This paper outlines how the Prop 103 rating system is slow, imprecise, and inflexible relative to other jurisdictions; examines the ways in which the ratemaking system has been rendered unpredictable; and details the form, function, and questionable value proposition of the rate-intervenor system. In so doing, the paper demonstrates that Prop 103 has created an insurance market that struggles to work efficiently even in the best of times and is virtually impossible to sustain in periods of acute stress.

Despite the current problems in California’s insurance market, industry critics argue that other states would be better off with regulations similar to those contained in Prop 103. A clear view of the results from California demonstrate that these arguments are false and misleading. Contrary to claims that Prop 103 saved Californians as much as $154 billion in auto insurance premiums from 1989 to 2015, we find that Californians would have saved nearly $25 billion if they had not passed Prop 103.

The paper concludes with a series of policy recommendations designed to inform both the ongoing implementation of Prop 103 by the California Department of Insurance, as well as other jurisdictions considering elements of a Prop 103 approach.

I. Introduction

The 1980s were a period of chaotic dislocation in the California automobile-insurance market.1 The California Supreme Court’s 1979 decision in Royal Globe Insurance created precedent that third parties could bring action against a tortfeasor’s insurer, even if they were not party to the insurance contract in question.2

Royal Globe Ins. Co. v. Superior Court, 23 Cal. 3d 880 (Cal. 1979), 153 Cal. Rptr. 842, 592 P.2d 329.

What followed was an explosion in insurance-related litigation, as the number of auto-liability claim filings in California Superior Court rose by 82% between 1980 and 1987, and the severity of claims rose by a factor of four.3 As would be expected, the state’s auto-insurance premiums likewise followed suit, rising 69.8% from $4.3 billion in 1984 to $7.3 billion in 1987.4Viscusi & Born, supra note 1, at 18.

This crisis in auto-insurance affordability came to a head in 1988, when among the 29 ballot initiatives California voters were presented in that November’s election were five separate questions dealing specifically with insurance issues.5 Two of these were broadly supported by the insurance industry: Proposition 104,6 which would establish a no-fault system for auto insurance and limit damage awards against insurers, and Proposition 106, which would set percentage-based caps on attorneys’ contingency fees.7

Gillam & Wolinsky, supra note 5.

Proposition 100, backed by the California Trial Lawyers Association, was proposed as a counter to Props 104 and 106; if it received more votes that those initiatives, it would have canceled the limits on both damage awards and contingency fees, as well as the proposed no-fault system.8 Proposition 101 would cap insureds’ ability to recover bodily injury damages, paired with a promised 50% reduction in the bodily injury portion of insurance premiums.9In the end, however, only one of the insurance measures was approved in the Nov. 8 election: Proposition 103, also known as the “Insurance Rate Reduction and Reform Act.” Authored by Harvey Rosenfield of the Santa Monica-based Foundation for Taxpayer and Consumer Rights (now known as Consumer Watchdog) and sponsored by Rosenfield’s organization Voter Revolt, Prop 103 carried narrowly with 51.1% yes votes to 48.9% against.10

Steve Geissinger, Californians Approve Auto Insurance Cuts, Insurer Files Lawsuit, Associated Press (Nov. 9, 1988).

Prop 103’s stated purpose was “to protect consumers from arbitrary insurance rates and practices, to encourage a competitive insurance marketplace.”11 Proponents of the measure claim they have achieved that, touting $154 billion of consumer savings over the first 30 years it was in effect.12

Among the specific changes mandated by the law were:

- California’s insurance commissioner, previously appointed by the governor, was made an elected position, chosen in the same cycle with the other state officers for a term of four years.

- Beginning in November 1988, all automobile and other property & casualty insurance rates were to be rolled back to 80% of their levels as of Nov. 8, 1987, and were to be held at such levels until November 1989.

- Rate increases and decreases were now subject to prior approval of

the elected insurance commissioner, replacing the “open competition”

system that had previously prevailed for 40 years under the

McBride-Grunsky Insurance Regulatory Act of 1947, which required only

that insurers submit rate manuals to the California Department of

Insurance (CDI).13

Cal. Ins. Code §1850-1860.3.

Public hearings were mandatory for personal lines increases of more than 7% and commercial lines increases of more than 15%, while others were at CDI’s discretion. - The law created a role at these hearings for “public intervenors,” who are empowered to file objections on behalf of consumers, with fees to be paid by the applicant insurance company.

- Prop 103 also established a rate-setting formula for auto insurance that mandated rates be based on an insured’s driving record, number of miles driven, and years of driving experience. While other factors could be considered, the burden would be on insurers to demonstrate they are statistically correlated with risk.

- Drivers with at least three years of driving experience, no more than one violation point during the previous three years, and no fault in an accident involving death or damage great than $500 must be offered a “good driver discount” that is at least 20% below the rate the driver would otherwise have been charged for coverage.

- The business of insurance was deemed subject to California antitrust, unfair business practices, and civil-rights law.

Because the law was subject to immediate and ongoing litigation, some provisions were only fully implemented years after the proposition’s passage. But notable among the law’s other provisions was Section 8(b), which rendered Prop 103’s text extraordinarily difficult to amend:

The provisions of this act shall not be amended by the Legislature except to further its purposes by a statute passed in each house by roll call vote entered in the journal, two-thirds of the membership concurring, or by a statute that becomes effective only when approved by the electorate.14

Stats. 1988, p. A-290.

Much has changed in the world, and in California’s insurance industry, since the passage of Prop 103, but the lion’s share of the law remains as it was in 1988.

II. The Recent History of California’s Insurance Market

The recent story of California’s property & casualty insurance market has been one of uncertainty and induced dysfunction.

Prior to the COVID-19 pandemic, California’s market was saddled by availability issues stemming from a series of historically costly wildfires. California homeowners insurers posted a combined underwriting loss of $20 billion for the massive wildfire years of 2017 and 2018 alone, more than double the total combined underwriting profit of $10 billion that the state’s homeowners insurers had generated from 1991 to 2016.15 Partly in response to those losses, as well as the inability to adjust rates expeditiously, the number of nonrenewals of California residential-property policies grew by 36% in 2019, and new policies written by the state’s residual-market FAIR Plan surged 225% that same year.16

To stanch the bleeding of admitted market policies into the FAIR Plan and the surplus-lines market, CDI in December 2019 invoked recently enacted statutory authority to issue moratoria barring insurers from nonrenewing roughly 800,000 policies in ZIP codes adjacent to specified major wildfires.17 As of November 2022, nearly 2.4 million policies statewide were in ZIP codes under nonrenewal moratoria, many of them added following additional catastrophic wildfires in 2020.18

During the COVID-19 pandemic, CDI instituted a rate freeze in auto insurance and accused the industry of profiteering. In June 2020, California Insurance Commissioner Ricardo Lara took credit for ordering $1.03 billion of premium refunds, dividends, or credits for auto-insurance policyholders, as well as “an additional $180 million in future rate increases that insurance companies reduced in response to the Commissioner’s orders.”19

In fact, most of the early rebates were voluntary, in line with similar voluntary rebates that insurers issued across the country.20 CDI would not publish its methodology for mandatory rebates until March 2021, at which point it declared that, rather than the 9% of premium that California auto insurers returned to policyholders from March through September 2020, they should have returned 17%.21 In October 2021, the California Court of Appeal ruled in State Farm General Insurance Co. v. Lara that Prop 103 did not actually give the commissioner authority to order the retroactive rate refunds.22

State Farm General Insurance Company v. Lara et al. (2021) 286 Cal. Rptr. 3d 124.

CDI was also slow to lift its rate freeze, even as the COVID-19 pandemic abated, and many employers ended work-from-home policies. From May 2020 until October 2022, CDI did not approve a single auto-insurance rate filing, even though more than 75% of the state’s auto insurers filed for an increase during that period.23 In the meantime, the “motor vehicle repair” component of the Consumer Price Index (CPI) jumped by 19.2% between July 2022 and July 2023, far outstripping the 3.2% hike in overall CPI.24

Consumer Price Index for All Urban Consumers (CPI-U): U.S. City Average by Detailed Expenditure Category, U.S. Bureau of Labor Statistics (Aug. 10, 2023), https://www.bls.gov/news.release/cpi.t02.htm.

With limited options on the pricing front, insurers have been forced to limit exposure in other ways. While California is a “guaranteed issue” state for private-passenger auto insurance, auto insurers are attempting to limit the policies they take on by, for example, limiting advertising. Insurance rating agency A.M. Best Co. reported that auto insurers cut their advertising budgets nearly 18% in the first half of 2022, compared with the same period in 2021.25 In other cases, insurers have taken to asking for more premium upfront, instead of allowing consumers to pay via monthly or other periodic installment plans.26

Meanwhile, as detailed more extensively in the sections below, the wildfire-driven homeowners-insurance crisis that began before the COVID-19 pandemic has itself grown to epidemic levels, highlighted by State Farm General’s 2023 decision to cease writing new business in the California market. That led the environmental news service ClimateWire to observe:

Experts say State Farm’s decision highlights a flaw in California policies that effectively blocks insurers from considering climate change in setting premiums and discourages them from seeking rate increases sufficient to cover the state’s growing wildfire risk. In addition, the policies have created insurance premiums that are far too low and are forcing insurers to pull back their coverage in California to remain profitable.27

California’s political leaders have also acknowledged the crisis. On Sept. 21, Gov. Gavin Newsom issued an executive order noting that insurance carriers representing 63% of the state’s homeowners insurance market had in recent months announced plans to either cease or limit writing new policies.28 He further announced that he was authorizing Insurance Commissioner Ricardo Lara to:

take prompt regulatory action to strengthen and stabilize California’s marketplace for homeowners insurance and commercial property insurance, and to consider whether the recent sudden deterioration of the private insurance market presents facts that support emergency regulatory action.29

Id.

For his part, Lara announced an emergency response plan that included:

[T]ransition[ing] homeowners and businesses from the FAIR Plan back into the normal insurance market with commitments from insurance companies to cover all parts of California by writing no less than 85% of their statewide market share in high wildfire risk communities. … ;

Giving FAIR Plan policyholders who comply with the new Safer from Wildfires regulation first priority for transition to the normal market, thus enhancing the state’s overall wildfire safety efforts;

Expediting the Department’s introduction of new rules for the review of climate catastrophe models that recognize the benefits of wildfire safety and mitigation actions at the state, local, and parcel levels; …

Holding public meetings exploring incorporating California-only reinsurance costs into rate filings;

Improving rate filing procedures and timelines by enforcing the requirement for insurance companies to submit a complete rate filing, hiring additional Department staff to review rate applications and inform regulatory changes, and enacting intervenor reform to increase transparency and public participation in the process …30

A. Problems With Rate Regulation Under Prop 103

Prop 103 charges California’s insurance commissioner with applying requirements articulated in the California Insurance Code and the California Code of Regulations to determine whether an insurer’s requested rate change is “excessive, inadequate or unfairly discriminatory.”31

Cal. Ins. Code §1861.137(b)

If the commissioner determines that a request is not “most actuarially sound,” he or she can require a rate reduction or reject a rate filing completely.32 Here, it should be noted that the “most actuarially sound” standard is unique to California, and is not applied by other states that employ prior-approval regulatory systems for rate review.The most obvious problem with rate regulation is that it restricts the availability of insurance. As the German economist Karl Henrik Borch put it in a landmark article on capital markets in insurance:

If premiums are low, the profitability of the insurance company will also be low, and investors may not be inclined to risk their capital as reserves for an insurance company. If the government imposes too low premiums, the whole system may break down, and high standard insurance may become impossible in a free economy.33

Karl Borch, Capital Markets and the Supervision of Insurance Companies, 31 Journal of Risk and Insurance 397 (Sep. 1974).

Insurers naturally respond to rate regulation by tightening their underwriting criteria, forcing some consumers to have to turn to the higher-priced residual market for coverage. In extreme cases, rate suppression can lead some insurers to exit the market altogether.

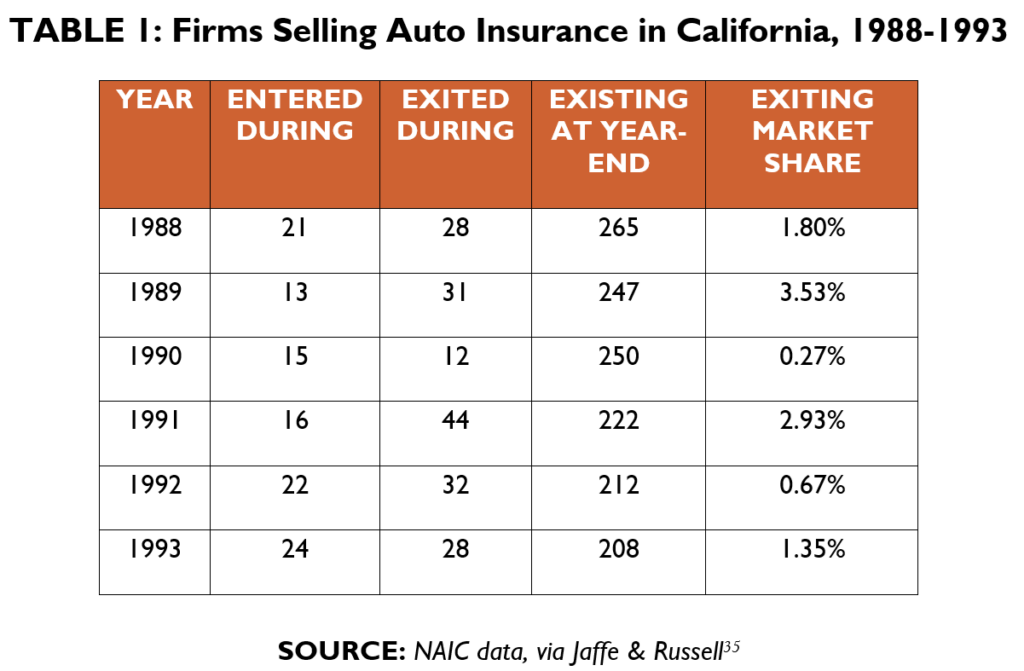

The empirical evidence of this effect is manifest. After California ordered mandatory 20% rate rollbacks following the passage of Prop 103 in 1988 (the effects of which were initially somewhat blunted by the courts), the number of insurers writing auto coverage in the state fell from 265 in 1988 to 208 in 1993.34

Dwight M. Jaffee & Thomas Russell, The Regulation of Automobile Insurance in California, in J.D. Cummins (ed.), Deregulating Property-Liability Insurance: Restoring Competition and Increasing Market Efficiency, American Enterprise Institute-Brookings Institution Joint Center for Regulatory Studies (2001).

35

Id.

More recently, Prop 103’s deleterious effects on the availability of coverage have manifested most obviously in decisions by major homeowners insurers to exit the market. In 2019, following the deadliest wildfire season in California history, the state’s homeowners insurers responded by nonrenewing 235,520 policies, a 31% increase from the prior year.36 In May 2023, California’s largest writer of homeowners insurance, State Farm General, announced it would halt the sale of new homeowners policies in the state.37 Six months earlier, in December 2022, California’s fourth-largest personal lines writer—Allstate—had likewise announced it would cease writing new policies,38 while Farmers, the second-largest writer, subsequently said it would limit it, too, would writing of new policies.39

While Prop 103 calls for property & casualty insurers to earn a “fair profit” rate of return of 10%, the industry has long reported that it finds it difficult to meet the California Department of Insurance’s requirements to justify rate increases, even when such increases would allow premiums to better reflect true risk.40 In fact, even after the state’s extreme wildfires in 2017 and 2018, and despite trailing only Hawaii in median home prices,41 Californians in 2020 paid an annual average of $1,285 in homeowners insurance premiums across all policy types—less than the national average of $1,319.42

As noted above, the homeowners-insurance availability crisis has become particularly acute in the wake of those devastating 2017 and 2018 wildfires. Under Prop 103, an insurer must justify its requested statewide premium for future wildfire losses based upon its average annual wildfire losses over the last 20 years.43

Cal. Code Regs. Tit. 10, § 2644.5.

But as demonstrated in Figure I, a look at the data from California’s homeowners-insurance market illustrates why such long-run averages are wholly inadequate to project future losses.44

Xu et al., supra note 15.

B. Catastrophe Models and Reinsurance

Insurers have access to tools like advanced wildfire catastrophe models that would allow them to project future wildfire losses in ways that consider both changing climactic factors and a given property’s proximity to fuel load.45

Robert Zolla & Melanie McFaul, Wildfire Catastrophe Models and Their Use in California for Ratemaking, Milliman (Jul. 21, 2023),

Such considerations are not currently permitted under California’s Prop 103 system, but nor are they explicitly barred, as such models largely did not yet exist in 1988. Indeed, the California Earthquake Authority uses catastrophe models to develop rates and mitigation discounts; determine the amount of claims-paying capacity the authority needs; and to estimate CEA losses after an event.46 Moreover, California has begun to take steps in the direction of permitting their use in certain limited contexts, including recent regulations requiring insurers to disclose to consumers their “wildfire risk score.”47 In July 2023, Insurance Commissioner Ricardo Lara hosted a workshop on catastrophe modeling and insurance, noting in a public invitation that:For the past 30 years, the use of actual historical catastrophe losses has been the method used for estimating catastrophe adjustments in the California rate-approval process. However, historical losses do not fully account for the growing risk caused by climate change or risk mitigation measures taken by communities or regionally, as a result of local, state, and federal investments. Catastrophe estimates based on historical losses only reflect losses after they occur. As a result of climate-intensified wildfire risk and continued development in the wildland urban interface areas, and recent increased efforts to mitigate wildfire risks, past experience may no longer reflect the current wildfire exposure for property owners and insurance companies.48

Prop 103 also probits insurers from using the cost of reinsurance as justification for rate filings.49

Cal. Ins. Code §623.

After a long period of “soft” pricing from 2006 to 2016, reinsurance rates for North American property-catastrophe risks more than doubled from 2017 to 2023, including a 35% year-over-year hike in 2023, according to reinsurance broker Guy Carpenter.50 When combined with prohibitions on the use of catastrophe models, this has essentially meant that California—a state that has long prided itself as being on the leading edge when it comes to its response to climate change—is effectively telling insurers to ignore the science.51Thus, unsurprisingly, denied the ability to charge rates that reflect the future risk of wildfire, admitted-market insurers have pulled back from the most at-risk areas. Ironically, this has meant a migration of policies to surplus lines insurers and to the California Fair Access to Insurance Requirements (FAIR) Plan, both of which are allowed to use catastrophe models in setting their premiums.

From 2015 to 2021, the number of FAIR Plan policies grew by 89.7%, in the process rising from 1.7% of the California homeowners insurance market to 3.0%.52 With just $1.4 billion in aggregate loss retention and facing the prospect of claims-paying shortfalls in the event of another major wildfire, the FAIR Plan recently filed a request for an average 48.8% increase in its dwelling fire rates.53

C. An Inflexible System

Prop 103 is also remarkably inflexible, particularly given provisions that make it exceedingly difficult to amend by legislative enactment. Any changes must not only pass by a two-thirds vote in both chambers of the California Legislature, but they must also be found to “further the purposes” of the proposition. As the 2nd District Court of Appeal wrote in the 1998 decision Proposition 103 Enforcement v. Quackenbush:

Any doubts should be resolved in favor of the initiative and referendum power, and amendments which may conflict with the subject matter of initiative measures must be accomplished by popular vote, as opposed to legislatively enacted ordinances, where the original initiative does not provide otherwise.54

Proposition 103 Enforcement Project v. Charles Quackenbush, 64 Cal. App.4th 1473 (Cal. Ct. App. 1998), 76 Cal. Rptr. 2d 342.

But with the bar to amendment set that high, it has proven to be effectively impossible for the law to respond to the enormous political, technological, and business practice changes that the insurance industry has undergone over the past 35 years.

In addition to the emergence of catastrophe models, discussed above, another significant tool that insurers have taken increasing advantage of in the years since 1988 is the use of credit-based insurance scores, particularly in auto insurance underwriting and ratemaking. Today, according to the Fair Isaac Corp. (FICO), 95% of auto insurers and 85% of homeowners insurers use credit-based insurance scores in states where it is legally allowed as an underwriting or risk-classification factor.55

But California is one of four states (along with Massachusetts, Hawaii, and Michigan) that does not permit their use,56 because CDI has not adopted regulations acknowledging credit history as a rating factor with “a substantial relationship to the risk of loss.” This is despite the Federal Trade Commission’s (FTC) finding that, in the context of auto insurance, credit-based insurance scores “are predictive of the number of claims consumers file and the total cost of those claims.”57

A similar disjunction between the inflexibility of Prop 103 and the emergence of new technologies can be seen in the development of “telematic” technologies that allow insurers to measure a range of factors directly relevant to auto-insurance risk, including not only the number of miles driven (a required rating factor under Prop 103) but also how frequently the driver engages in sudden stops or rapid acceleration, as well as how often he or she drives after dark or in high-congestion situations.58

In July 2009, CDI adopted an amendment to the state insurance code that permitted the use of telematics devices to verify mileage for the purpose of advertise “pay per-mile” rates.59

10 CCR § 2632.5.

But other regulations in the California code limit the ability to use telematics to offer “pay-how-you-drive” products that have become popular in other jurisdictions. For example, insurers are currently prohibited from collecting vehicle-location information, which rules out rating on the basis of driving in congested areas.6010 CCR § 2632.5(c)(2).F.5.B.

Moreover, because the regulations do permit rating on the basis of the severity and frequency of accidents in the ZIP code where a vehicle is garaged,6110 CCR § 2632.5(d)(15-16)

identical drivers who spend equivalent time driving in congested areas may be charged different rates, with a suburban commuter earning a discount relative to an urban commuter.Research by Jason E. Bordoff & Pascal J. Noel finds the status quo is that low-mileage drivers cross-subsidize high-mileage drivers,62 and that about 64% of Californians would save money if they switched to a per-mile plan.63 The president of the California Black Chamber of Commerce has also argued that telematics offers a potential solution to problems of bias in underwriting, given evidence that drivers from predominantly African-American communities are quoted premiums that are 70% higher than similarly situated drivers in predominantly white communities.64

By voluntarily downloading an app to their smartphone, a driver agrees to allow an insurer to measure data about (and only about) their driving habits. This includes behaviors like hard braking and distracted driving. Based on that data an insurance company can assess how much of a risk the driver poses and offer fair insurance, free of bias and inflation, that the driver may choose to purchase.65

Id.

III. Prop 103 Rate Review in Practice

Dynamic aspects of insurance loss events and claim costs impose expenses on insurers if they cannot respond nimbly in matching rate to risk. Prop 103 and similar approaches to price regulation restrain insurers’ ability to adjust to new information, thereby causing an increase in price, a decrease in availability, or both. Rate suppression occurs when regulators deny rate filings that request adequate and non-excessive rates. Examples of extreme rate suppression have rarely lasted very long. Insurers exit suppressed markets, leaving consumers with fewer choices and higher prices.

While the last section examined some of the high-level issues created by the Prop 103 system, in this section, we draw from empirical data and recent legal precedent to demonstrate how the Prop 103 process, as applied by the CDI, has in practice amplified these dislocations in ways that have proven extraordinarily counterproductive.

A. Ratemaking as Market-Conduct Examination

Filing for rates under Prop 103 is a complex and costly enterprise. The discretion that CDI maintains and the ever-present risk of intervention by a third parties means that swift and predictable resolution is the exception, not the rule.

Further complicating ratemaking in California is the intrinsically political nature of the relationship between the insurance commissioner and regulated entities. California’s commissioner is one of 11 state insurance regulators in the United States to face direct election.66 Thus, particularly in times of market strain or when policyholders are confronted with availability challenges or rate increases, the commissioner faces political incentives to pressure insurers to acquiesce to popular—if not market-based—demands. As a result, the ratemaking process can be misused as a proxy venue for larger ongoing disputes between the commissioner and insurers. Two recent cases highlight this phenomenon.

1. Rulemaking by ratemaking proceeding

State Farm General (SFG)—a California entity separate from the larger State Farm Mutual, which was established to cover non-automobile lines—sought a rate increase of 6.4% in 2015. Consumer Watchdog intervened, CDI rejected the proposed increase, and the matter went to a hearing before a CDI administrative-law judge. The department’s hearing officer subsequently issued a far-reaching opinion, which was adopted by the commissioner, ordering SFG to retroactively reduce its rates and issue refunds, based on a novel reading of Prop 103 that erased the difference between the balance sheets of a particular insurer and the larger group of which it is a part for purposes of ratemaking.

Faced with a foundational reinterpretation of insurance law created in the process of seeking a rate, SFG appealed to California courts, where it ultimately prevailed, after a years-long protracted lawsuit and subsequent CDI appeal.67

State Farm General Insurance Company v. Lara et al. (2021) 286 Cal. Rptr. 3d 124.

While resolving open questions about a state’s ratemaking process is appropriate fodder for any department to undertake, the broader context in which then-Insurance Commissioner Dave Jones—who launched what would ultimately be a failed bid to be elected California’s attorney general in 201868—pursued the action against SFG speaks to a different motivation. Indeed, SFG had just one year prior sought and received a rate increase using the same formula subsequently rejected by CDI. To wit, the basis of CDI’s resistance was not the degree of the rate increase in question, but was instead premised upon a broader question of law.

CDI has broad rulemaking authority and, when necessary, can seek legislative amendment to ensure that the laws governing ratemaking protect California consumers. But the department also retains substantial leverage to secure acquiescence from insurers when it pursues novel ratemaking interpretations in the context of a particular rate application. This approach may be effective, but it frustrates well-established norms for creating rules of general applicability and deprives the industry as a whole of due process. Worse still, when it engages in facial abuses of its already broad discretion, the CDI undermines the Prop 103 ratemaking system’s ability to prevent dislocation between price and risk.

2. Corporate governance by ratemaking proceeding

The ratemaking process under Prop 103 is likewise susceptible to being used to direct the behavior of firms beyond the scope of ratemaking itself. Predictably, delays in the ratemaking proceeding on account of nonprice factors trigger the same market-skewing dynamics and due-process issues discussed above. Intervenors like Consumer Watchdog have sought, e.g., to prevent Allstate from receiving a mere 4% rate increase in its homeowners book on the basis of the firm’s decision to limit its exposure to the California market more broadly.69 In that case, the long-time intervenor alleged that ceasing to sell insurance—an underwriting determination—has an impact on rates and that as a result, the decision to cease offering coverage is itself a ratemaking action demanding review by California Department of Insurance.

To its credit, the department maintained that inactivity by a business does not constitute the use of an unapproved rate. But Consumer Watchdog’s broad reading of the acceptable scope of matters judicable in a ratemaking proceeding is no doubt borne directly of previous experiences in which insurers were made to acquiesce to demands related to business practices more broadly.

B. Prop 103’s Dead Letter Deemer

Rate-approval delays have become a hallmark of the Prop 103 system, as well as the resulting asymmetry between rate and risk. But as originally presented to California voters, the law envisioned that rates would be deemed accepted if no action were taken by the CDI for 60 or 180 days.70

CIC Section 1861.05.

Indeed, Prop 103 included this “deemer” provision because a reasonable speed-to-market for insurance products also protects consumers.The law’s deemer provision has been effectively rendered moot in practice because, as a matter of course, the CDI requests that firms waive the deemer. If the deemer is not waived, the CDI has two options: approve the rate or issue a formal notice of hearing on the rate proposal. Because the CDI is unable to complete timely review of filings within the deemer period, it always elects to move to a rate hearing. In effect, CDI turns every rate filing without a deemer waiver into an “extraordinary circumstance.”71

CIC 1861.065(d).

In practice, it has proven exceedingly challenging for petitioners to navigate the manner in which rate hearings—the nominal guarantors of due process—are conducted. The administrative law judges (ALJs) that oversee these proceedings are housed within the CDI. The hearings themselves take a broad view of relevance that drive up the cost of participation. Upon ALJ resolution, the commissioner can accept, reject, or modify the ALJ’s finding. There is little practical upside for an insurer to move to a hearing against the CDI.

Wawanesa General Insurance Co. offers a case study in the differences between how Prop 103 was drafted and the way it is currently enforced. After initially waiving the law’s deemer, Wawanesa reactivated the deemer in a 2021 private-passenger auto filing.72

SERFF WAWA-133081408.

In so doing, Wawanesa elected to move to a hearing by the CDI. Ultimately, from start to finish, its December 2021 rate filing was not approved until March 2023—15 months after it was brought forward. Ultimately, unable to get the rate it needed in a timely manner, Wawanesa’s U.S. subsidiary was acquired by the Automobile Club of Southern California.73Thus, in practice, insurers are faced with a starkly practical choice. One option is to waive their right to timely review of rates, and hope that they gain approval in, on average, six months. The alternative is to move to a formal hearing and reconcile themselves with the fact that approval, if forthcoming, will take at least a year. The system of due process originally contemplated by Prop 103 simply bears no relationship with the system as it operates today.

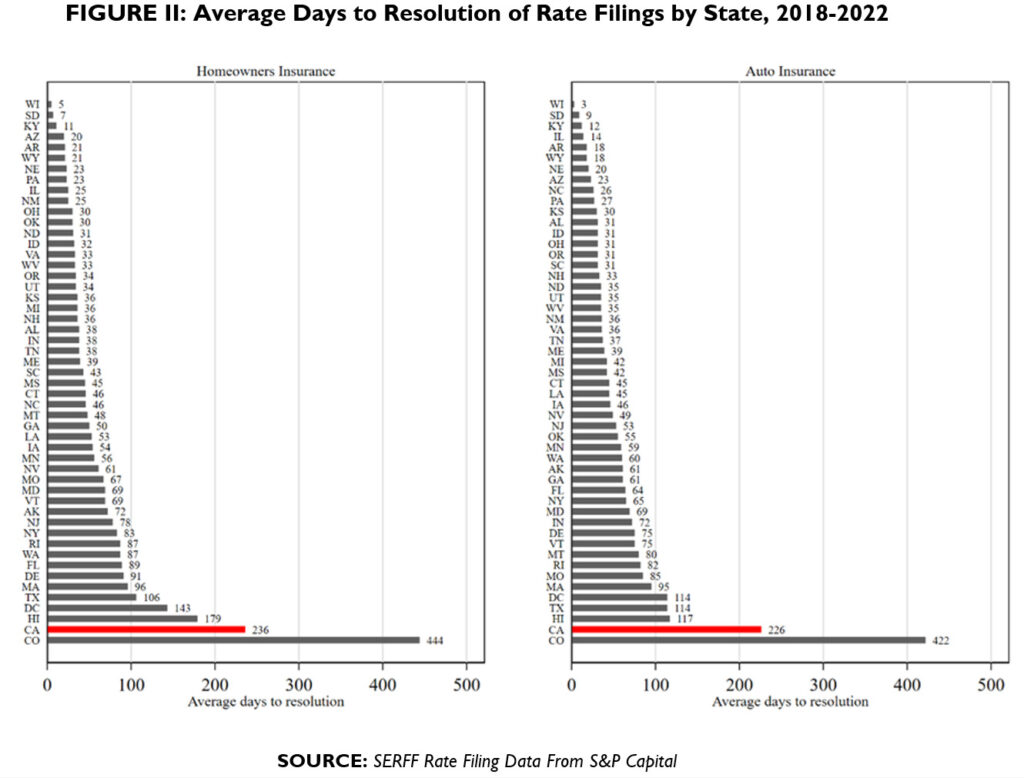

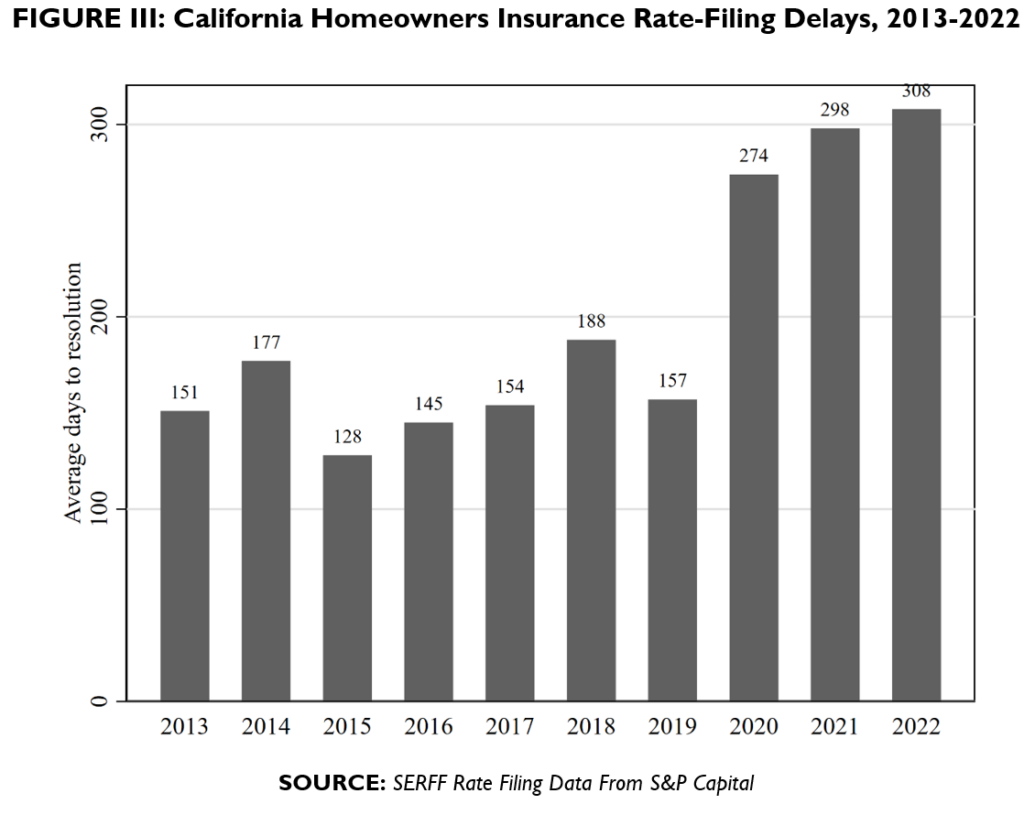

Figure II shows the average number of days between submission and resolution of rate filings in each state (including the District of Columbia as a state, for these purposes). With a five-year average filing delay of 236 days for homeowners insurance and 226 days for auto insurance, California ranks 50th in each category, responding more slowly than all states except Colorado. Although the average delay is affected somewhat by extreme-outlier observations, California’s rank is unchanged if we instead use the median delay.74

The median delay for homeowners rate filings in California is 198 days. For auto insurance rate filings, it is 185.5 days.

Another troubling aspect of California’s sluggish regulatory system is that it appears to be getting slower over time. Obviously, California has been relatively slow to resolve rate filings since Prop 103 took effect. In recent years, however, the average delay has increased, as wildfire losses and market conditions (e.g., inflation and the cost of capital) have increased the cost of providing insurance. Figure III shows the annual average number of days between filing and resolution of rate changes for homeowners insurance in California. The average delay from 2013 to 2019 was 157 days. For the last three years, the average delay has increased to 293 days.

C. The Intervenor Process

CDI’s ability to review rate filings in a timely manner is further constrained by Prop 103’s intervenor process. Intervenors are granted petitions to intervene, as a matter of right, on any rate filing. Personal-lines filings that request a rate increase of 6.9% or more (or 14.9% or more in commercial-lines filings) are subject to mandatory hearings, if requested, while the decision to grant hearings for those filings below 6.9% (or 14.9% for commercial lines) are at the commissioner’s discretion. Naturally, many personal lines insurers opt to file below that threshold, even if they actually require rate increases substantially in excess of 6.9%, simply to avoid dealing with intervenors (although many rate filings at or below 6.9% do also have intervenors).

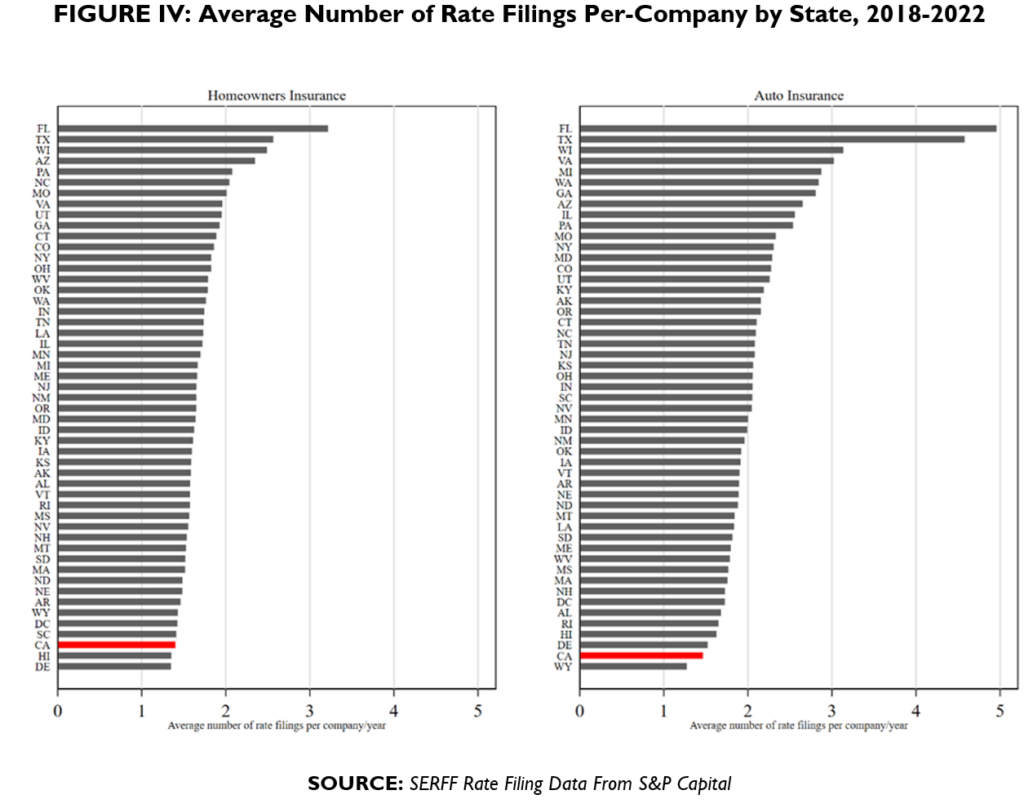

The intervenor process has proven both costly and time-consuming. According to CDI data, since 2003, intervenors have been paid $23,267,698.72, or just over $1 million annually, for successfully challenging 177 filings.75 While the process results in CDI receiving more filings to review than it otherwise would, the total number of filings it must review is significantly less than other jurisdictions (see Figure IV).

Intuitively, we can assume that states cannot change rates as frequently when rate filings take longer to resolve. Figure IV confirms this assumption, demonstrating the average number of rate filings made per-company in each state for homeowners and automobile insurance from 2018 to 2022. Over the last five years, California ranks 49th in the number of homeowners-insurance rates filed, and 50th in the number of auto-insurance rates filed.

D. Rate Suppression Under Prop 103

While a slow regulatory system limits the efficiency of insurance markets, a system that suppresses rates will also inhibit deployment of capital, ultimately reducing the number of insurers who choose to participate.

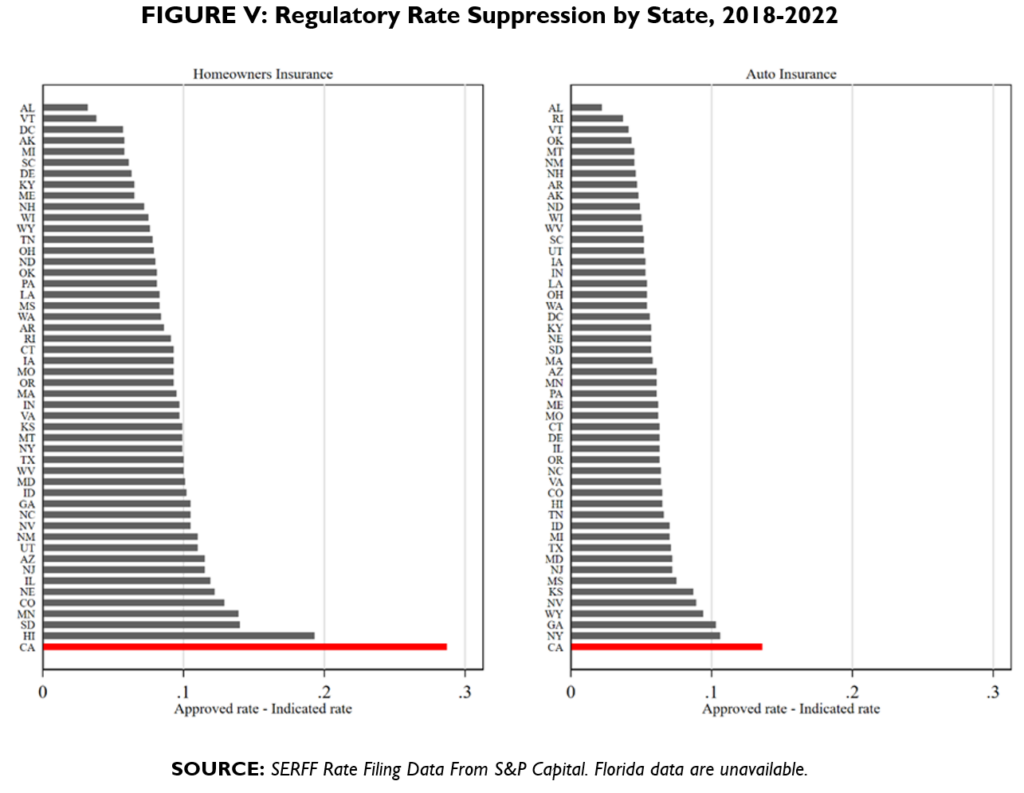

For example, if an insurer’s rate analysis indicates that a 40% increase is required for rates to be adequate, and the regulator instead approves only a 15% increase, the effect of rate suppression is (40%–15%=) 25%. In this category, California again ranks 50th, approving rates that are, on average, 29% (homeowners) and 14% (auto) less than the actuarially indicated rate supported by the analysis in the filing.76

Data from Florida are not available for this measure; therefore, California ranks 50th out of 50 jurisdictions.

Figure V, which measures the difference between the actuarially indicated rate and the rate approved by regulators, demonstrates that California’s regulatory system under Prop 103 is suppressive. Although it is common for insurers to request rate changes below the indicated rates for strategic reasons, the measure would not differ consistently across states in the absence of suppressive rate regulation.

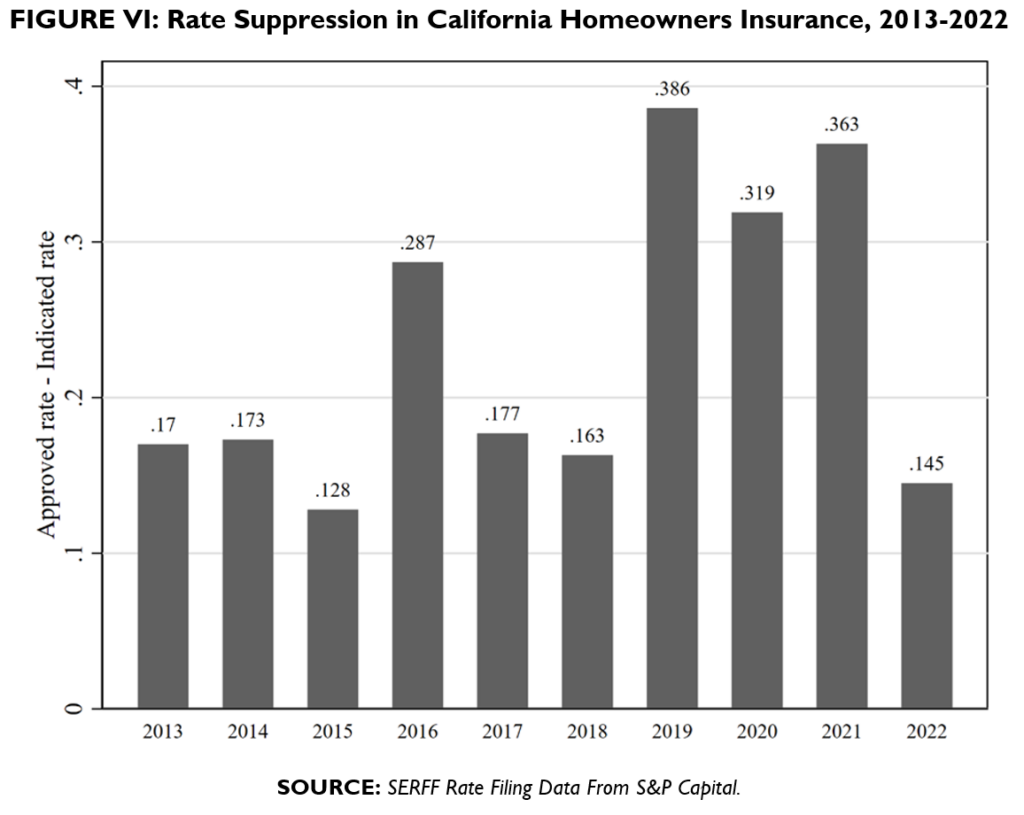

Similar to the growing chasm of filing delays observed in Figure III, Figure 7 shows that rate suppression in California homeowners insurance has risen in response to the unprecedented wildfire losses incurred in 2017 and 2018. Although the level of rate suppression moderated somewhat in 2022, the average level of regulatory rate suppression for 2013 through 2018 was 18%, while the average for 2019 through 2022 is 30%. Moreover, at 14.5% in 2022, California is more than one standard deviation (3.6%) above the mean (9.8%) and ranks 45th among the 50 jurisdictions reporting data.

In summary, the rate-filing data clearly show that California’s regulatory system under Prop 103 is expensive and slow, and that it is currently causing unsustainable rate suppression, especially in the homeowners line.

IV. The Impact of Prop 103 on Other States

Some of Prop 103’s effects have arguably spilled over to other jurisdictions, either directly—via states adopting similar regulatory regimes—or indirectly. Recent research by Sangmin S. Oh, Ishita Sen, & Ana-Maria Tenekedjieva suggests that there is a significant indirect effect in the form of rate suppression in California and other “high-friction” states leading to cross-subsidies among policyholders of multi-state insurers and, ultimately, “distortions in risk sharing across states.”77

First, rates have not adequately adjusted in response to the growth in losses in states we classify as “high friction”, i.e. states where regulation is most restrictive. Second, in low friction states rates increase both in response to local losses as well as to losses from high friction states. Importantly, these spillovers are asymmetric: they occur only from high to low friction states, consistent with insurers cross-subsidizing in response to rate regulation. Our results point to distortions in risk sharing across states, i.e. households in low friction states are in-part bearing the risks of households in high friction states.78

Id. at 1.

In other cases, the impact of Prop 103 has largely taken the form of political influence. As demonstrated in the previous section, states like Colorado, Maryland, and Hawaii have followed California’s model of extended rate-review processes that significantly slow product approvals.

Among the first states to respond to Prop 103 with its own similar regulatory system was New Jersey, which in 1990 passed the Fair Automobile Insurance Reform Act. Under terms of the law, effective April 1992, every admitted writer of automobile insurance in the state would be required to offer coverage for all eligible persons, with only a select group of motorists—including those convicted of driving under the influence or other automobile-related crimes, those whose licenses had been suspended, those convicted of insurance fraud, and those whose coverage had been canceled for nonpayment of premium—deemed ineligible.79

While the law nominally permitted insurers to earn an “adequate return on capital” of 13%, several companies would sue the state on grounds that the New Jersey Department of Banking and Insurance did not approve rate requests sufficient to meet that threshold.80

High Court Upholds N.J. Surcharges on Insurers, A.M. Best Co. (Mar. 19, 1996).

In addition, the state assessed surcharged on insurers to close a $1.3 billion funding gap for the state’s Joint Underwriting Authority.81Anthony Gnoffo Jr., NJ, Insurers Near Deal to Close State Fund Gap, The Journal of Commerce (1994).

As in California, New Jersey saw the exit of 20 insurers the state’s auto-insurance market in the decade after the Fair Automobile Insurance Reform Act’s passage. When the state later liberalized its regulatory system with passage of the Auto Insurance Reform Act in June 2003, the number of auto writers more than doubled from 17 to 39 and thousands of previously uninsured drivers entered the system.82

A similar effect was seen in South Carolina, where a restrictive rating system in the 1990s had forced 43% of drivers into residual market policies undergirded by a state-run reinsurance facility.83 After adopting a liberalized flex-band rating law in 1999, as in New Jersey, the number of insurers offering coverage in South Carolina doubled,84

Tennyson, supra note 10.

the residual market shrank (it is, today, only 0.007% of the market),85 and overall rates actually fell.Even in Massachusetts, which retains a fairly restrictive rate-approval process, reforms passed in April 2008 to allow insurers to submit competitive rates (they were previously set by the commissioner for all carriers) had a notable impact. Within two years of the reforms, rates had fallen by 12.7% and a dozen new carriers began offering coverage in the state.86 Because it is still a very regulated state, Massachusetts still has a relatively large residual market. According to data from the Automobile Insurance Plan Service Office (AIPSO), in 2022, 3.38% of Massachusetts auto-insurance customers had to resort to the residual market, the second-highest rate in the nation.87

AIPSO, supra note 13.

But before 2008, Massachusetts’ residual-market share was routinely in the double digits.While those states that have opted to copy the California model have largely lived to regret it, others continue to explore the imposition of Prop 103-like regimes. Oregon lawmakers, for example, have repeatedly put forward legislation that would place the insurance industry under the state’s Unlawful Trade Practices Act, granting customers the right to sue for damages beyond even the face value of their policies, and third parties to bring private rights of action against insurers with whom they have no contractual relationship.88

But perhaps the most notable recent proposal to shift to a Prop 103-like system is Illinois’ H.B. 2203,89

Motor Vehicle Insurance Fairness Act, H.B. 2203, Illinois 103rd General Assembly.

which would effectively transform the state from the most open and competitive insurance market in the country to one of the most restrictive. If approved, the legislation would require every insurer seeking to offer private passenger motor-vehicle liability insurance in the state to file a complete rate application with the Department of Insurance, which once again would be empowered to approve or disapprove rates on a prior-approval basis. The bill also would prohibit insurers from setting rates based on any “nondriving” factors, including credit history, occupation, education, and gender.As in California, the measure would also create a new system for public intervenors in the ratemaking process, stipulating that “any person may initiate or intervene in any proceeding permitted or established under the provisions and challenge any action of the Director under the provisions.”90

Id.

Illinois is currently somewhat of an outlier in effectively having no formal rate-approval process at all. In 1971, the Illinois General Assembly neglected to extend legislation enacted a year earlier to create “file-and-use” system, and the state has continued on without any insurance rating law for more than half a century.91

V. Estimating the Cost of Prop 103 in California and Other States

For the last two decades, proponents of Prop 103 have asserted that the ballot measure saved Californians as much as $154 billion in auto-insurance premiums from 1989 to 2015. Further, they claim that other states could have saved nearly $60 billion per-year over the same period by adopting insurance regulations similar to Prop 103.92 As David Appel has noted, the analysis supporting these claims is flawed.93 In the 20 years since industry critics began making this claim, however, no one has performed the correct analysis. Here, we perform an object analysis and draw dramatically different conclusions.

The analyses performed and cited by Prop 103’s proponents assume that insurance premiums are a function of the prior year’s premiums.94 This approach is invalid, because insurance premiums are instead a function of expected losses. For example, if a policy covering a $200,000 house has a lower premium than a policy covering a $500,000 house, that alone would not tell us whether the first policy is a better deal than the second. Equivalently, we cannot tout the value of automobile insurance without comparing premiums to losses.

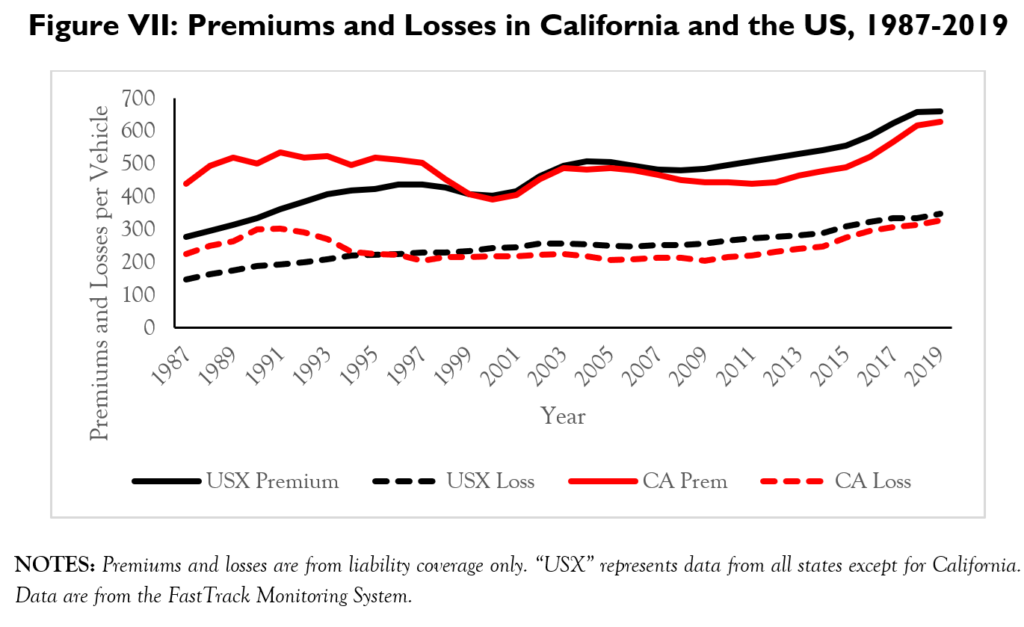

Figure VII shows that premiums in California and in other states (USX) largely follow losses. Moreover, when insurance companies make rate filings asking state insurance departments to approve new rates, regulators evaluate them based on their similarity to past losses and loss trends. Therefore, a more appropriate method of creating a counterfactual comparing the results obtained under one state’s regulatory approach to the insurance premiums that would be generated in other states is to apply the ratio of premiums to losses from one state to the losses of the other states, as in Equation 1:

Where USX PremiumCA is the estimate of USX premiums if we impose the effects of California’s price controls on the rest of the country.

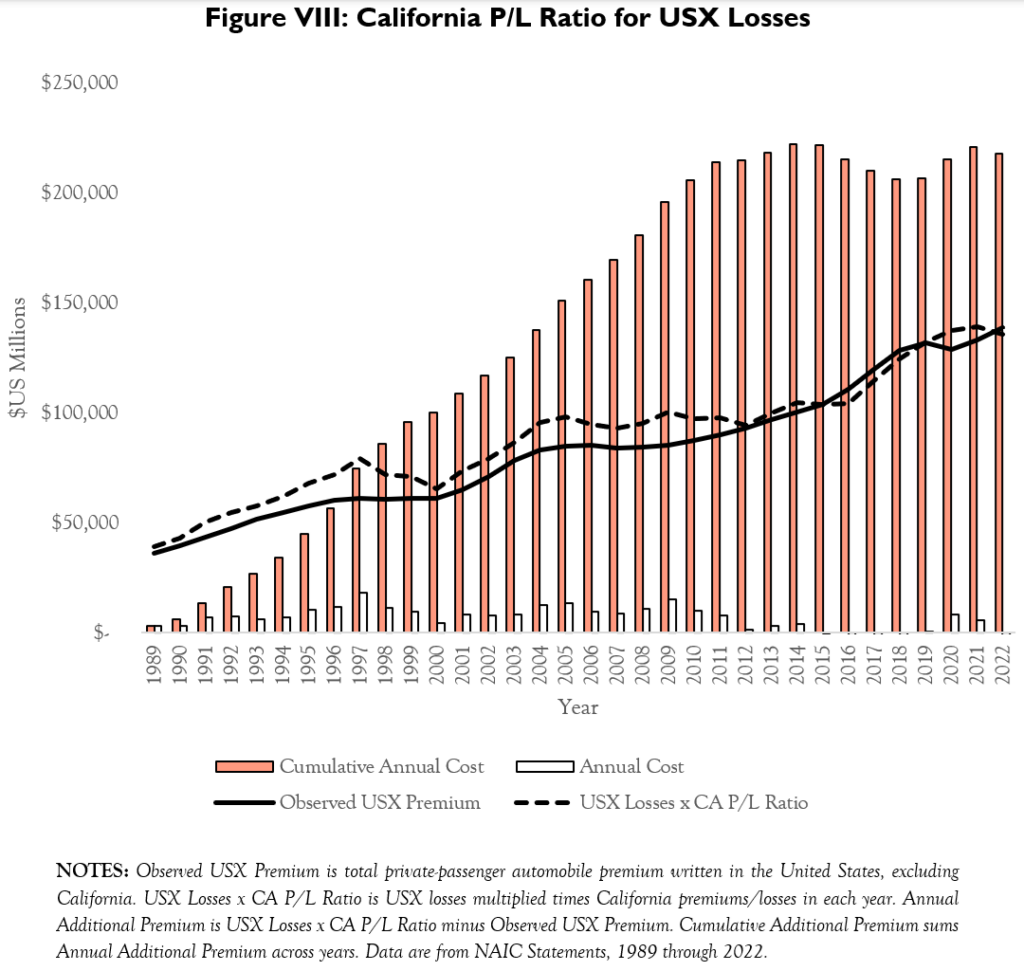

Figure VIII shows the results from solving Equation 1. In stark contrast to claims made by proponents of Prop 103, we find that if the rest of the country (USX) had passed Prop 103 in 1989, consumers would have paid more than $218 billion in additional auto insurance premiums. Likewise, results from solving Equation 2:

Where CA PremiumUSX is the estimate of California premiums if we remove the effects of Prop 103 on California, indicate that Californians would have saved nearly $25 billion if they had not passed Prop 103. In light of these findings, regulators should be appropriately skeptical of claims that price controls reduce insurance premiums.

VI. Recommended Reforms

It is difficult, but not impossible, to amend Prop 103. Indeed, many reforms may be enacted by updating administrative interpretation alone. What follows is, first, a list of reforms that CDI could champion (some of which are included, in varying forms, in Commissioner Lara’s emergency plan) to improve speed-to-market, procedural predictability, and rate accuracy. Second is a list of structural reforms that would require legislative approval.

A. Interpretive Reforms

1. Fast-track noncontroversial filings

As discussed above, Prop 103 grants CDI discretion on whether to convene public hearings on rate changes of less than 7% for personal lines or 15% for commercial lines. When the commissioner grants such hearings, it adds expense, administrative burden, and delays to very modest changes in product offerings. Not only is this problematic as a matter of substance, we have shown that the data on delays in rate-filing approvals demonstrate that CDI is routinely violating the explicit text of Prop 103, which requires that “a rate change application shall be deemed approved 180 days after the rate application is received by the commissioner” unless the commissioner either rejects the filing or there are “extraordinary circumstances.”95

Consumer Watchdog, supra note 11.

CDI not only can, but must act to uphold this provision of the law.To do so, the CDI should entertain adopting a rate-approval “fastlane” premised on firms submitting filings that use actuarial judgments that embrace consumer-friendly assumptions. That is, if a filing is made on the basis of the least-inflationary or least-aggressive loss-development assumptions, CDI should undertake a light-touch review focused on rate sufficiency to expedite the approval process. This approach has the benefit of increasing both the predictability and speed of the ratemaking process.

2. Refocus rate proceedings

If CDI were to adopt a narrower reading of the universe of rate-related issues appropriate for adjudication in a ratemaking proceeding, it would have the important benefit of limiting the universe of issues susceptible to controversy. In so doing, insurers and the department will better be able to focus on the resolution of rate applications in a timely manner that allows price to reflect risk. Relatedly, the department should continue to constrain intervenors from conflating rate-related and non-rate-related issues in the service of broader policy objectives.

3. Transparency

There is no single cause for California’s substantial delay in approving rates, but it is clear that the state’s unique intervenor system shapes both insurer and CDI behavior in ways that were not immediately cognizable when the law was adopted. One way to ensure that speed-to-market improves over the long term is to better understand the value that intervenors offer, and to ensure that intervenor engagement is both efficient and effective.

At the moment, CDI publishes quantitative data concerning intervenor compensation and rate differentiation in intervenor proceedings.96 But while this is helpful in conveying the scope of intervenor efforts, the data fail to capture the value actually provided by intervenors in the ratemaking process. The qualitative contribution made by intervenors is obscured by the fact that none of their filings appear publicly on SERFF. Not only is this an aberration relative to other proceedings before the CDI, but there could be significant value in getting greater transparency from the intervenor process, given the delays and direct costs related to intervention.

For one, allowing the Legislature and the public to assess the substantive value of intervenor contributions would ensure not only substantial due-process protections for filing entities, but would also ensure that consumers are afforded a high level of representation in proceedings. For instance, such transparency would function as a guarantor that intervenor filings are not otherwise duplicative of CDI efforts. It would therefore allow the public to assess whether intervenors are diligent in their efforts on their behalf.

Therefore, CDI should consider requiring intervenors to have their filings reflected on SERFF. Doing so would cost virtually nothing and would redound to the benefit of all parties. And it should be noted that, as this paper was going to press, CDI had started to post intervenor filings (Petitions to Intervene and Petitions for Hearing) for public access.

And beyond simply making intervenor contributions more transparent, CDI should exercise its discretion to reduce and sometimes reject fee submissions due to the lack of significant or substantial contribution. The department has long rubber-stamped fee requests, thereby creating incentives for unnecessary and costly delays in reviews and in actuarially justified rate increases.

4. Embracing catastrophe models

Another reform that may be possible to enact via regulatory action is allowing the use of wildfire catastrophe models to rate and underwrite risk on a prospective basis. As mentioned above, there is precedent for such interpretation, as the FAIR Plan and the California Earthquake Authority already use catastrophe models for similar purposes. The Legislature could contribute to this process by appropriating funds for a commission to formally review the output of wildfire models, much as the Florida Commission on Hurricane Loss Projection Methodology (FCHLPM) does for hurricane models.97 A formal review process could also provide insurers with the certainty they would need to justify investing in refined pricing strategies without fear that regulators will later reject the underlying methodology.

B. Legislative Reforms

The following proposals would require one of the exceptional legislative processes outlined above. Under the most common, a bill would have to clear both chambers of the Legislature by a two-thirds majority, and courts would ultimately be called on to rule in any challenges (and there will be challenges) whether the measure “furthers the purpose” of Prop 103.

But there is another option. The Legislature could also, by simple majority vote, opt to pass a statute that becomes effective only when approved by the electorate. This path has largely been eschewed by past would-be reformers, who have considered the odds long that the voting public would choose to make changes to Prop 103.

That may once have been obviously true, but as the California market continues to struggle, and as banks and property owners find it impossible to secure coverage at any price, it is difficult to say with certainty what voters would do. Prop 103 itself passed narrowly, against the backdrop of an insurance market crisis. As we find ourselves in yet another such crisis, anything may be possible.

1. Insurance Market Action Plan

One option to address availability concerns and shrink the bloated FAIR Plan would be for the Legislature to revive the Insurance Market Action Plan (IMAP) proposal that the Assembly passed by a 61-3 margin in June 2020.98

A.B. 2167, California Legislature 2019-2020 Regular Session.

Similar to the “takeout” program used successfully to depopulate Florida’s Citizens Property Insurance Corp., under IMAP, insurers that committed to write a significant number of properties in counties with large proportions of FAIR Plan policies would be allowed to submit rate requests that considered the output of catastrophe models and the market cost of reinsurance. In addition, FAIR Plan assessments should be applied as a direct surcharge, not subject to CDI approval, to ensure that there is no unfair subsidization of the highest risks, as well as to guard against the burden of assessments contributing to the insolvency of private insurers.

IMAP filings would also receive expedited review by the insurance commissioner, which could alleviate the speed-to-market issues highlighted in Section III.

2. Telematics

There has also been some legislative interest in broadening the availability of telematics. In 2020, Assemblymember Evan Low (D-Campbell) and then- Assemblymember Autumn Burke (D-Marina Del Rey) co-authored an op-ed in which they called telematics “a sensible and fair approach” and encouraged CDI to continue to explore the issue with stakeholders.99

Prop. 103 was passed in an age before cell phones, GPS Navigation and many other technological advancements. Its interpretation does not allow companies to rate customers on their driving behavior. Prop. 103 relies heavily on demographic factors, rather than basing your rate on how you drive.

VI. Conclusion

As demonstrated in this paper, claims about Prop 103’s savings to consumers100

Consumer Federation of America, supra note 12.

must be taken with an enormous grain of salt. Prop 103’s suppression of property-insurance rates in the private market has contributed to an availability crisis and the shunting of policyholders into the surplus-lines market and the California FAIR Plan, both of which will inevitably have to raise rates accordingly to be able to meet their obligations. This displacement into what are intended to be mechanisms of last resort also deprives consumers of the protections ordinarily offered in the admitted market.- Robert Hunter, Tom Feltner, & Douglas Heller, What Works: A Review of Auto Insurance Rate Regulation in America and How Best Practices Save Billions of Dollars Consumer Federation of America (Nov. 2013), available at http://consumerfed.org/wp-content/uploads/2010/08/whatworks-report_nov2013_hunter-feltner-heller.pdf; see also Hunter & Heller, supra note 92.

How to afford fire insurance in California

For the last five years (from August 2018 to August 2023), Californians have experienced an average of over 5,000 wildland fires per year, burning an average of over 800,000 acres per year.

Just how bad were these wildfires for property owners? In just the past two years – from 2022 to 2023 – wildfires in California caused at least $3.2 billion in damage. And California isn’t the only state with wildfire concerns. Most western states, including Arizona, have seen more wildfires – even Florida saw several wildfires in 2022. More recently, Hawaii was devastated by a series of deadly wildfires on the island of Maui.

The rising costs of damage from wildfires mean that insurance providers are paying more in claims, which means they’re turning to their own insurance providers – called reinsurers – with more claims on their policies. Essentially, everyone is feeling the pinch.

To manage their risk exposure, reinsurers typically have to raise prices for their customers. Their customers, the insurance companies, then have to raise prices for homeowners or send nonrenewal notices, effectively canceling homeowner's policies. In fact, nonrenewals in California have increased more than 31 percent since 2019.

This is a problem for those who live in areas with wildfire risk exposure. The good news is that if your current insurance provider sends you a nonrenewal notice or raises premiums beyond what you can afford, there are steps you can take to keep yourself covered for wildfire damage.

Is fire insurance mandatory in California?

Before we get to the steps for finding more affordable fire insurance, let’s first address another question: do you even need it? While there is no state-level law requiring homeowners to have fire insurance, most mortgage lenders do require it as a condition of the loan. So if you have a mortgage on your house, it’s safe to assume that fire insurance is mandatory.

Even if you own your home free and clear, carrying fire insurance is the safest option. Fires can spark from shorted-out appliances, lightning storms, downed powerlines, tossed cigarettes, and dozens of other activities you have no control over. Fire insurance helps make sure you and your family can live normally even if a disaster hits.

Fire insurance is included in most standard homeowners insurance policies.

Now let’s take a look at how California homeowners can find affordable fire insurance.

1. Shop around for fire insurance

It’s a good idea to shop around for fire insurance even if you don’t live in California – or if you live in a region of the state that’s not prone to wildfires. It’s a good idea to shop around for just about everything, and fire insurance is no exception.

-

Search online. Some newer insurance providers sell directly to customers and don’t work with outside brokers to keep costs low. (While we are a direct-to-consumer insurance provider, we don’t currently offer coverage in California.)

-

Ask friends for recommendations. If you have friends and family in California, ask them about companies they’ve worked with to insure their homes. Once you have a list of recommendations, start gathering quotes to compare.

Ideally, once you’ve explored additional coverage options, you’ll find one that works for your home and your budget. If you don’t, move on to the next step.

2. Consider non-admitted fire insurance carriers

Most of the insurance companies you’ve heard of are “admitted” carriers, which means they’ve been approved by a state’s insurance department. If the carrier went bankrupt, the state would cover payments for claims on active policies.

Non-admitted carriers are not approved by a state’s insurance department. They’re less regulated so they can take on more risk. Non-admitted insurance carriers may be the only workable solution for someone in a high-risk wildfire zone.

Non-admitted carriers are also sometimes called surplus carriers or specialty carriers. If you’re unable to find fire insurance through admitted carriers for your California home, see what some non-admitted carriers offer.

3. Call the California insurance helpline

If even after considering non-admitted carriers you can’t find a fire insurance policy to cover your home, it’s time to call California’s insurance helpline at 1-800-927-HELP.

This line is maintained by California’s Department of Insurance and is designed to help California residents figure out how to find adequate insurance. A helpline worker might point you toward the FAIR plan.

4. Consider California FAIR Plan fire insurance

The California Fair Access to Insurance Requirements (FAIR) plan is an insurer of last resort. Its website explicitly states that it is designed only for those homeowners who have made a “diligent effort” to find coverage elsewhere.

If you can’t find that coverage, though, the FAIR plan may be able to offer the fire insurance you need. If you do go this route, it’s important to understand a few things:

-

You’re responsible for knowing how much coverage you need. When you work with a private insurer, you can usually work with a representative who helps you understand the value of your home, your risk exposure, and the amount and type of coverage you need. With the FAIR plan, you have to calculate how much coverage to get on your own. You may want to work with an insurance broker to do this. Luckily, the California FAIR plan’s website explains how to find a broker.

-

California FAIR plan fire insurance doesn’t cover theft or liability. In this way, it’s different from standard homeowners insurance, which includes coverage for both theft and liability. If you purchase a policy through the FAIR plan, be sure to consider additional coverage to manage your other risks.

-

California FAIR plan coverage is limited to $1.5 million. If the cost of rebuilding your home is more than that, you’ll have to find supplemental coverage or attempt to self-insure by saving enough cash to make up the difference.

What to expect from California fire insurance prices